Circuits de commercialisation et certification biologique dans le secteur français des fruits

- Type de publication : Article de revue

- Revue : Systèmes alimentaires / Food Systems

2021, n° 6. varia - Auteurs : Aubert (Magali), Enjolras (Geoffroy), Bouhsina (Zouhair)

- Résumé : Cet article examine l'influence des circuits de commercialisation sur l'adoption de l'agriculture biologique. L'originalité de cette étude est de considérer à la fois les circuits alimentaires courts et longs ainsi que leur hétérogénéité. Elle utilise une enquête représentative des exploitations fruitières françaises. Les résultats montrent que les filières courtes et longues favorisent la production biologique dans la mesure où les producteurs connaissent la destination de leur production

- Pages : 167 à 194

- Revue : Systèmes alimentaires

- Thème CLIL : 3306 -- SCIENCES ÉCONOMIQUES -- Économie de la mondialisation et du développement

- EAN : 9782406127055

- ISBN : 978-2-406-12705-5

- ISSN : 2555-0411

- DOI : 10.48611/isbn.978-2-406-12705-5.p.0167

- Éditeur : Classiques Garnier

- Mise en ligne : 05/01/2022

- Périodicité : Annuelle

- Langue : Anglais

- Mots-clés : agriculture biologique, circuit de commercialisation, fruit, certification, France.

Marketing channels

and organic certification

in the French fruit sector

Magali Aubert

UMR 1110 MOISA,

Univ Montpellier, CIRAD, CIHEAM-IAMM, INRAE,

Institut Agro, Montpellier, France

Geoffroy Enjolras

CERAG, Univ. Grenoble Alpes

Zouhair Bouhsina

UMR 1110 MOISA,

Univ Montpellier, CIRAD, CIHEAM-IAMM, INRAE,

Institut Agro, Montpellier, France

Introduction

Recent sanitary crises have strengthened the requirements of consumers in terms of food safety and quality management (Richards et al., 2013). Such an evolution is characterized inter alia by the development of quality standards (Giraud-Héraud et al., 2006), the promotion of organic farming (Sylvander and Schieb-Bienfait, 2006; Tuomisto et al., 2012) and the development of alternative food supply chains (Penker, 2006; Renting et al., 2003; Venn et al., 2006).

168The road to organic farming takes the form of a supervised process which leads to an official certification (Burton et al., 2003; Heckman, 2006). From conventional to organic practices, there are several indicators related to the adoption of environmentally-friendly practices. Adoption can be measured either through the quantities of pesticide used (Aubert and Enjolras, 2014), the implementation of integrated pest management techniques (Fernandez-Cornejo, 1996; Fernandez-Cornejo and Ferraioli, 1999; Galt, 2008; McNamara and Keith Douce, 1991) or even labeled organic farming practices (Aubert and Enjolras, 2016; Moustier and Thi Tan Loc, 2013). The organic farming label plays a key role in signaling trust attributes to consumers regarding the quality of agricultural products and processes (Lee et al., 2020).

The adoption of organic farming is driven by several factors (Hazell et al., 2010). The aforementioned studies consider a set of explanatory variables which consider the farm structure (acreage and production), its financial situation (profitability and indebtedness) and the farm holder’s characteristics (age and education). A specific feature of the marketing of organic products is an active involvement of producers and consumers (Lombardi et al., 2015; Taghikhah et al., 2019).

While consumers praise the quality of organic products, producers are encouraged to choose marketing channels that properly value this quality (Asian et al., 2019; Hwang and Chung, 2019). In this line, short food supply chains such as direct selling and processing convey an image of quality and sustainable food as well as a perception of proximity (Chiffoleau and Dourian, 2020; Kottila and Rönni, 2008; Renting et al., 2003). The values and attributes carried by these marketing channels contribute to reinforcing trust between consumers and producers (Galli et al., 2015), which explains their expansion dynamics in recent years (Moati and Ranvier, 2005; Cavaliere et al., 2016).

For those reasons, the existing literature emphasizes the existence of a strong link between short food supply chains and the quality of agricultural produces (Broderick et al., 2011; Galt, 2008; Maréchal and Spanu, 2010; Souza Monteiro and Caswell, 2009; Zhou et al., 2011). The display of both “organic farming” and “short food supply chains” labels presupposes compliance with a set of specifications which in return helps reduce asymmetric information effects as defined in Akerlof (1970).

169In practice, the organic production is sold through a wide range of marketing channels (Agence Bio, 2020). We notice there is insufficient consideration in the literature of the influence of marketing channels other than direct and retail selling on the adoption of an organic certification. More precisely, to the best of our knowledge, no work considers the diversity of marketing channels available to producers, especially regarding long channels. This paper aims to fill this gap by studying the influence of marketing channels on the adoption of organic farming by French fruit producers, by differentiating different types of long channels.

Our analysis uses data from the ‘Orchard Survey’ (Enquête Vergers), carried out in 2012 by the French Statistical and Forecasting Service (SSP). This sample of French fruit-producing farms provides detailed information relating to both the adoption of organic farming and marketing channels. French fruit production encompasses a broad spectrum of products ranging from the most perishable ones (e.g., apricots, peaches) to storable ones (e.g., apples, nuts).

Fruit production faces a challenge relating to its ecological sustainability. While fruits represent less than 1% of the agricultural area farmed nationwide, they account for more than 5% of phytosanitary expenditures. With pesticides expenses of close to €600 per hectare, this sector is the most intensive consumer of pesticides (Butault et al., 2012). Phytosanitary requirements have therefore been increasing following the implementation of the EcoPhyto I (2008), Ecophyto II (2015) and Ecophyto II+ (2018) frameworks, the objectives of which are to reduce the intensity of pesticide use in French agriculture.

According to the ‘Orchard Survey’, direct selling represents about 5% of the volume of fruits marketed in France. This figure should be seen in relation to the fact that in 2010, 27% of fruit producers were selling all or part of their produce through this marketing channel (French Ministry of Agriculture, 2010). The fact remains that a majority of fruit production is sold using long or indirect supply chains. Producer organizations remain the predominant marketing channel, accounting for about 50% of volumes marketed in France. They enable producers to manage their risks better by planning production in accordance with demand and concentrating supply (European Commission, 2018). Wholesalers represent about 25% of volumes traded while forwarders 170account for 15% of traded volumes. Less than 5% of the produce marketed is intended to export or processing.

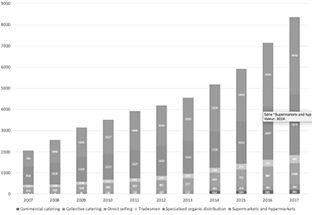

According to recent data from the Agence Bio (2020), the market share of organic farming produce in 2019 represented about 26% of total production of fruits in France. Specialty stores sold the largest share (43%), while supermarkets accounted for 35% and direct selling 22%. Figure 1 summarizes the evolution of organic sales by marketing channels. It shows that while sales of organic products are increasing rapidly, the proportion of each distribution channel remains more or less the same over time.

Key: Sales are expressed in millions of euros.

Source: Agence Bio (2020).

Fig. 1 – Evolution of organic sales by marketing channels from 2007 to 2017.

In order to measure the influence of the marketing channels on organic farming, we use an econometric logit model which considers the diversity of existing marketing channels. Obtaining an organic farming label is indeed the result of a long certification process that may be driven by the involvement in specific supply chains.

171This article is structured as follows. In the first section, we develop a literature review. In the second section, we present both the empirical approach and the empirical strategy. In the third section, we present the results using descriptive statistics and econometric models. In the fourth section, we conclude and provide some perspectives.

1. Literature review

In this section, we present a literature review which emphasizes the potential influence of the choice of marketing channel and key control variables on the adoption of organic farming. Testable hypotheses are then formulated which will be tested using empirical modeling.

1.1. Marketing channels and organic farming

According to the French Ministry of Agriculture, short food supply chains are defined by the existence of no more than one intermediary between the producer and the consumer (Barry, 2012). This definition corresponds primarily to direct selling where there is no intermediary, the producer thus selling his production directly to consumers. It also includes indirect selling where there is only one intermediary in the chain, for instance when the producer sells his products to supermarkets and hypermarkets.

Given the longstanding trend in favor of the adoption of organic farming, it has been observed that farmers receive a price premium when they obtain access to organic markets (Läpple and Rensburg, 2011). This premium is all the more important as organic farming is associated with low yields and production volumes (Łuczka and Kalinowski, 2020). A similar premium exists for farms selling through short food supply chains because of the small number of intermediaries in the chain (Hardesty and Leff, 2010). Consequently, farmers adopting both short food supply chains and organic farming are likely to exhibit higher profits (Tundys and Wiśniewski, 2020; Uematsu and Mishra, 2012).

Similarly, organic farming and short food supply chains share social and territorial values appreciated by producers (Renting et al., 2003). 172Costa et al. (2014) show that these values are also shared by consumers who are looking for produce complying with certain quality requirements. Demand would then lead to an increased quality of supply, directly through marketing channels. In this context, both farmers who sell their produce directly and retailers who sell this produce indirectly drive the development of organic farming (Smith, 2006).

As indirect channels, supermarkets allow to a large number of customers to purchase organic produce because of their capacity to propose a wide range of these goods (Martinez et al., 2010). They therefore create incentives for farmers to propose differentiated produce to consumers. Moreover, the development of organic supermarkets with an established reputation favors the sale of agricultural products via this channel (Steffen and Doppler, 2019).

Long food supply chains include more than one intermediary between the producer and the consumer. They encompass identified long channels where production is destined to be processed. Even if there are several intermediaries, the producer is aware of the final destination or use of his produce. These chains also include unidentified long channels whereby the producer sells his produce to producer organizations, wholesalers and forwarders. In this case, the producer does not know the final destination or intended use of his production. Whatever the channel, long supply chains are governed by specifications which impose quality and traceability standards (Scandella and Christy, 2011).

Long food supply chains include producer organizations (POs), which were formally created by the Council Regulation (EC) No 2200/96 of 28 October 1996 on the common organization of the market in fruit and vegetables. One of their main objectives is to centralize all the productions of their members, even small farms, to deal with the concentration of supply. POs improve producers’ competitive conditions (Camanzi et al., 2011) and performance (Michalek et al., 2018). They organize the traceability of produce and provide the necessary means for the implementation of environmentally friendly practices (Coppola and Ianuario, 2017; Dubuisson-Quellier et al., 2006).

As intermediaries in the fruit and vegetables sector, wholesalers implement a residual control plan for pesticide residues. They can ensure the traceability of their supplies by imposing specifications on their suppliers (Michel, 2014). Another important marketing channel is that 173of forwarders. Because they are very often involved in the importation of goods, they usually set up a voluntary self-monitoring plan designed to minimize health risks (Rouvière and Latouche, 2014).

Michelsen (2001) emphasizes that organic farming is enforced by public regulations, which paves the way for the development of organic farming through long marketing channels. While Ilbery et al. (2014) show that short food supply chains are a favored means of adopting organic farming, consumers’ expectations may also lead to demand for organic produce through long national chains when enough information is provided on the organic produce.

From this literature review, we notice that short food supply chains are the most compatible with organic farming on the basis of shared values, especially proximity and trust. Hence, we assume the following research hypothesis.

H1. Farms involved in short marketing channels are more likely to adopt organic farming than farms involved in long marketing channels.

Insofar as short food supply chains are divided between direct and indirect ones, the physical proximity between producers and consumers induced by direct selling appears as a strong incentive for farms to adopt quality production labels. We thus assume the following research hypothesis.

H2. Farms involved in direct selling channels are more likely to adopt organic farming than farms involved in indirect selling channels.

Given that some long supply chains can be qualified as identified while others can be qualified as unidentified, incentives for environmentally-friendly practices are not the same, which has in turn consequences for the adoption of labels such as organic farming. We thus assume the following research hypothesis.

H3. Farms involved in long identified marketing channels are more likely to adopt organic farming than farms involved in long unidentified marketing channels.

1741.2. Control variables and organic farming

Because individual farms are easier to manage, they may be better suited to complying with organic farming regulations (Läpple and Rensburg, 2011). This is confirmed by Darnhofer et al. (2005) who asserts that the conversion to organic farming is an individual decision.

H4. Individual farming is more likely to support the adoption of organic farming than farms operating in a collective form.

Burton et al. (1999), Läpple and Rensburg (2011) and Aubert and Enjolras (2017) find that farmers who operate small farms are more likely to adopt organic farming and they propose different explanations. Burton et al. (1999) point out that farmers involved in organic farming believe that a large farm size is bad for the environment. Läpple and Rensburg (2011) underline the agility of small farms to adopt innovations in opposition to Diederen et al. (2003) who showed that innovation is more commonly adopted by larger farms.

H5. Small farms support the adoption of organic farming.

Ilbery et al. (2014) explain that organic farming is mainly associated with consumers’ expectations, which differ from one region to another. They also argue that the choice of marketing channels is driven by regional considerations, which is in line with observations made by Barham et al. (2004).

H6. The adoption of organic farming differs according to regional particularities.

Darnhofer et al. (2005) show that farm specialization is less important than the farmers’ personal values in the choice of organic farming. When a farm converts to organic farming, all crops are concerned (Buck et al., 1997) and no distinction should be made between the specific types of produce (Lamine, 2011). With regard to fruit production, practices do not emphasize differences between orchard products when adopting organic farming (Lind et al., 2004; Weibel, 2002).

175H7. The adoption of organic farming does not differ according to fruit specializations.

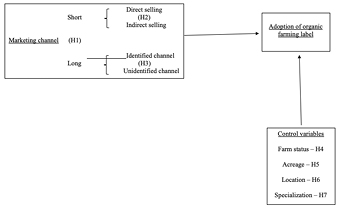

The research hypotheses are summarized in Figure 2.

Fig. 2 – Research hypotheses.

2. Empirical approach

In this section, we present the specific database used and its importance in understanding farmers’ choices concerning marketing channels. We also illustrate the econometric model to be estimated.

2.1. Database

The empirical analysis developed in this paper is based on an ‘Orchard Survey’ (Enquête Vergers), carried out in 2012 by the French Statistical and Forecasting Service (SSP). This survey is designed to meet one of 176the main objectives of the EcoPhyto frameworks: the characterization of phytosanitary practices. Hence, this database makes it possible to assess both the level of use of phytosanitary products (through the number of treatments) and the implementation of alternative practices. This database is also the only one that considers the diversity of food supply chains.

All farms producing fruit are considered and the sampling technique is quite complex to ensure that results are representative of a specific fruit in a specific region. Two sub-populations are considered: on the one hand farms producing apples, apricots, peaches, kiwis, citrus fruits, nuts or plums and, on the other hand, farms producing pears, cherries and table grapes. For each type of produce, farms are surveyed if they farm at least 2.47 acres of the former and at least 1.24 acres for the latter.

For each farm, the database references both the produce farmed and the associated marketing channels. We then know the acreage and the volumes sold using each channel. In addition, the database provides information on the individual farms such as the usable agricultural area, the geographical location (administrative region), and the status (Table 1).

Tab. 1 – List of variables.

|

Variables |

Definition |

Unit |

|

Organic farming |

The farmer adopts organic farming certification |

Dummy |

|

Marketing channels |

||

|

Direct selling |

The producer sells all or part of his produce directly to consumers |

Dummy |

|

Indirect selling |

The producer sells part or all of his produce to supermarkets or hypermarkets |

Dummy |

|

Identified long channel |

The producer sells all or part of his produce to processors |

Dummy |

|

Unidentified long channel |

The producer sells all or part of his produce to intermediaries: producer organizations, wholesalers or forwarders |

Dummy |

|

Farm status |

||

|

Status |

The farm is individual or operates within a group of farms |

Dummy |

| 177

Farm location |

||

|

Aquitaine |

The farm is located in Aquitaine |

Dummy |

|

Languedoc-Roussillon |

The farm is located in Languedoc-Roussillon |

Dummy |

|

Limousin |

The farm is located in Limousin |

Dummy |

|

Midi-Pyrénées |

The farm is located in Midi-Pyrénées |

Dummy |

|

Centre-Val de Loire |

The farm is located in Centre-Val de Loire |

Dummy |

|

Provence-Alpes-Côte d’Azur |

The farm is located in Provence-Alpes-Côte d’Azur |

Dummy |

|

Rhône-Alpes |

The farm is located in Rhône-Alpes |

Dummy |

|

Other region |

The farm is located in another region |

Dummy |

|

Farm specialization |

||

|

Main production |

Apples, apricots, pears, peaches, plums, cherries, kiwis, table grapes, citrus fruits |

Dummy |

|

Other control variables |

||

|

Acreage |

The physical size of the farm |

Hectare |

This database is both the most precise available at the farm and plot levels and the most comprehensive available to us. We consider and differentiate all types of fruit in our empirical approach, irrespective of their relative importance in terms of area farmed. One exception that should be highlighted is the case of citrus fruits, because of the low number of producers surveyed. To guarantee the confidentiality of citrus fruit producers, we decided not to analyze this population.

We consider each type of fruit production in an independent manner. The aim is to analyze to the extent to which the adoption of organic farming certification is conditioned by marketing channels, regardless of the fruit considered. Considering potential fruit particularities enables us to assess the validity of results from one type of produce to another. As a matter of fact, some fruits are non-perishable and can be stored, such as apples, while others are perishable and therefore require a local marketing, such as apricots. We also distinguish stone fruits and pome fruits. The results may also be interpreted in terms of fruit production as a whole.

178The marketing channels considered in the database include producer organizations, wholesalers, direct selling, supermarkets and hypermarkets, forwarders and processing. Based on these categories, we decided to classify them in terms of ‘distance’, measured by the number of intermediaries between consumers and producers (Ritchie and Brindley, 2000).

Two main categories are therefore identified: short food supply chains and long food supply chains. Each of these categories can in turn be divided into two subcategories according to our research hypotheses. Within short food supply chains, we differentiate direct from indirect selling and within long chains, identified from unidentified long channels. Since the destination of the produce is not necessarily exclusive, producers can sell all or part of their production to one channel or decide to combine several channels. Accordingly, we take a dichotomous approach to each channel. This approach considers the producers’ involvement in different marketing channels, whatever the quantity sold through each channel.

Finally, the database provides information about the adoption, or not, of organic farming certification. No additional information is provided about the relative importance of the farmed area dedicated to organic farming. This methodological choice aims to assess the importance of marketing strategies on productive ones, independently of the individual characteristics of farmers or the structural characteristics of their farms.

2.2. Econometric modeling

The adoption of organic farming is considered through a dummy variable. In order to understand the extent to which farmers are more likely to adopt this certification, we implement a logit model. We acknowledge that productive and marketing decisions made by farmers are somehow related given that they represent strategic issues for farmers. We choose to focus only on the link between marketing channels and organic farming given that obtaining an organic farming label is a result of a long certification process that may be driven by the involvement in specific supply chains.

Formally, the model considered can be defined as follows:

where: α represents the constant, β, θ, Z and W are the coefficients associated with the marketing channels, and more precisely with direct selling, indirect selling, identified long-channels and unidentified long-channels respectively, ζ is the coefficient associated with farm status, γ and δ are the coefficients associated with control variables (acreage and geographical location respectively) and ε is the error term.

While the marketing channels and farm status are at the heart of our study, we also consider certain control variables (acreage and location), because these factors are highlighted by the literature as leading to the adoption of certification.

3. Results

The results take into account the variety of the French fruit production by considering each type of fruit as well as the overall production. They show that the adoption of organic farming certification varies from one type of produce to another. Some farmers appear to be more inclined to implement such certification. Apples, pears, kiwis and citrus fruits would seem to be more prone to such certification than other types of produce such as cherries, peaches and plums (Table 2).

Tab. 2 – Characterization of each type of fruit production.

|

Apples |

Apricots |

Pears |

Peaches |

Plums |

Cherries |

Kiwis |

Table grapes |

Citrus fruits |

All fruits |

|

|

Acreage (%) |

36.80% |

12.60% |

4.99% |

10.90% |

17.11% |

7.76% |

3.45% |

4.82% |

1.58% |

100.00% |

|

Number (%) |

21.99% |

12.91% |

9.40% |

7.74% |

13.55% |

18.81% |

5.02% |

9.53% |

1.04% |

100.00% |

|

Organic producers (%) |

9.81% |

6.95% |

8.45% |

4.09% |

5.10% |

3.33% |

11.34% |

7.30% |

10.50% |

5.90% |

Source: Orchard Survey (2012).

180The marketing channels also differ from one type of produce to another. Since producers can sell through different channels, the relative importance of each one is measured through the volume sold through each channel (Tables 3 and 4). By considering both organic farming certification and the marketing channels, we observe that conventional farmers are over-represented in the “unidentified long channel”. Farmers involved in organic farming appear to be relatively more involved in short food supply chains and in identified long-channels.

Tab. 3 – Relative importance of types of fruit in total fruit acreage.

|

Direct selling |

Indirect selling |

Identified long channel |

Unidentified long channel |

Total |

||

|

Apples |

Conventional |

29.00% |

6.49% |

15.58% |

48.93% |

100.00% |

|

Organic farming |

36.69% |

10.07% |

25.47% |

27.77% |

100.00% |

|

|

Apricots |

Conventional |

15.66% |

5.90% |

5.62% |

72.82% |

100.00% |

|

Organic farming |

19.03% |

7.08% |

16.37% |

57.52% |

100.00% |

|

|

Pears |

Conventional |

29.61% |

6.48% |

12.90% |

51.02% |

100.00% |

|

Organic farming |

39.72% |

7.48% |

18.22% |

34.58% |

100.00% |

|

|

Peaches |

Conventional |

34.20% |

7.58% |

3.12% |

55.10% |

100.00% |

|

Organic farming |

29.07% |

9.30% |

12.79% |

48.84% |

100.00% |

|

|

Plums |

Conventional |

8.92% |

2.50% |

2.45% |

86.13% |

100.00% |

|

Organic farming |

20.90% |

4.48% |

0.75% |

73.88% |

100.00% |

|

|

Cherries |

Conventional |

25.15% |

4.14% |

2.92% |

67.79% |

100.00% |

|

Organic farming |

33.33% |

7.80% |

8.51% |

50.35% |

100.00% |

|

|

Kiwis |

Conventional |

14.10% |

6.06% |

0.70% |

79.14% |

100.00% |

|

Organic farming |

27.66% |

14.18% |

4.96% |

53.19% |

100.00% |

|

|

Table grapes |

Conventional |

12.81% |

4.19% |

8.26% |

74.73% |

100.00% |

|

Organic farming |

25.47% |

9.32% |

10.56% |

54.66% |

100.00% |

Source: Orchard Survey (2012)

181Tab. 4 – Marketed quantities according to the marketing channel,

produce and type of farming.

|

Direct selling |

Indirect selling |

Identified long channel |

Unidentified long channel |

||||||

|

Mean |

Std deviation |

Mean |

Std deviation |

Mean |

Std deviation |

Mean |

Std deviation |

||

|

Apples |

Conventional farming |

236.8 |

637.4 |

171.2 |

1,276.0 |

99.7 |

821.7 |

3,496.2 |

7,738.5 |

|

Organic farming |

215.9 |

501.2 |

98.3 |

401.1 |

125.8 |

508.5 |

1,914.1 |

6,777.0 |

|

|

Tests of equality |

*** |

*** |

*** |

*** |

*** |

*** |

|||

|

Apricots |

Conventional farming |

16.0 |

70.7 |

33.2 |

253.5 |

4.8 |

34.9 |

583 |

1139 |

|

Organic farming |

10.9 |

31.5 |

10.2 |

53.1 |

5.2 |

15.2 |

166.5 |

227 |

|

|

Tests of equality |

* |

*** |

*** |

*** |

*** |

*** |

*** |

||

|

Pears |

Conventional farming |

45.7 |

129.1 |

31.6 |

185.6 |

25.4 |

122.7 |

524.9 |

1,070.9 |

|

Organic farming |

40.1 |

71.0 |

17.9 |

108.2 |

29.7 |

180.9 |

391.8 |

808.0 |

|

|

Tests of equality |

*** |

*** |

* |

*** |

|||||

|

Peaches |

Conventional farming |

86.9 |

441.4 |

153.2 |

2,123.8 |

15.7 |

245.1 |

1,258.6 |

3,422.4 |

|

Organic farming |

41.5 |

95.5 |

7.3 |

33.0 |

10.2 |

41.5 |

585.1 |

973.9 |

|

|

Tests of equality |

*** |

*** |

*** |

*** |

*** |

*** |

*** |

||

|

Plums |

Conventional farming |

5.3 |

39.2 |

5.6 |

102.9 |

11.3 |

258.7 |

505.2 |

917.5 |

|

Organic farming |

7.9 |

25.4 |

8.6 |

51.4 |

0.1 |

1.1 |

277.8 |

771.1 |

|

|

Tests of equality |

*** |

*** |

*** |

*** |

*** |

** |

|||

| 182

Cherries |

Conventional farming |

5.6 |

24.0 |

2.1 |

19.5 |

4.9 |

61.3 |

59.87 |

174.1 |

|

Organic farming |

3.3 |

7.6 |

1.3 |

8.7 |

1.0 |

4.4 |

29.71 |

74.21 |

|

|

Tests of equality |

*** |

*** |

*** |

*** |

*** |

* |

*** |

||

|

Kiwis |

Conventional farming |

25.0 |

188.7 |

18.7 |

118.9 |

0.1 |

1.8 |

620.6 |

1181.1 |

|

Organic farming |

55.6 |

145.3 |

48.5 |

159.7 |

0.8 |

4.6 |

448.2 |

716.9 |

|

|

Tests of equality |

*** |

*** |

*** |

** |

** |

*** |

|||

|

Table grapes |

Conventional farming |

7.3 |

38.1 |

4.8 |

43.0 |

7.9 |

45.6 |

236.9 |

390.3 |

|

Organic farming |

12.1 |

36.3 |

11.1 |

56.4 |

6.5 |

36.2 |

139.4 |

233.4 |

|

|

Tests of equality |

*** |

*** |

*** |

*** |

|||||

Source: Orchard Survey (2012).

Note: Exporters have been omitted because the number of observations is not sufficient for the statistical analysis. Tests of equality refer respectively to the T-test for equality of means and the F-test for equality of standard deviations between conventional and organic farming.

Key: *, ** and *** denote significance at the 10%, 5% and 1% levels respectively.

The distribution of organic farming among the French regions highlights certain differences (Table 5). For instance, organic apple production tends to be under-represented in the major fruit producing regions. This result is similar to overall fruit production, which can be linked to the importance of apple production in total fruit production. Conversely, organic apricot production is concentrated in certain regions, such as Languedoc-Roussillon and Provence-Alpes-Côte d’Azur, which are located in the South of France. For all types of produce except apples, farms are for the most part not operated individually, and this proportion increases for organic farms. Organic farming tends to rely on a personal initiative. This individual dynamic goes hand in hand with membership of producer organizations in the case of apple production.

183Tab. 5 – Farm location and status.

|

Location |

Status |

|||||||||

|

Aquitaine |

Languedoc-Roussillon |

Limousin |

Midi-Pyrénées |

Centre-Val de Loire |

Provence-Alpes-Côte d’Azur |

Rhône-Alpes |

Other region |

Individual farm |

||

|

Apples |

Conventional farming |

7.50% |

5.93% |

7.82% |

13.09% |

13.23% |

20.19% |

16.09% |

16.14% |

44.15% |

|

Organic farming |

6.03% |

6.44% |

3.26% |

12.46% |

14.66% |

15.13% |

17.14% |

24.88% |

48.61% |

|

|

Apricots |

Conventional farming |

29.07% |

2.64% |

14.80% |

51.91% |

0.81% |

59.80% |

|||

|

Organic farming |

1.98% |

43.67% |

1.28% |

20.24% |

32.19% |

0.64% |

53.57% |

|||

|

Pears |

Conventional farming |

3.80% |

4.98% |

1.83% |

4.61% |

13.09% |

31.56% |

23.66% |

16.46% |

46.13% |

|

Organic farming |

2.17% |

3.20% |

1.52% |

19.06% |

32.07% |

23.92% |

18.06% |

47.22% |

||

|

Peaches |

Conventional farming |

6.69% |

35.86% |

11.55% |

15.16% |

25.96% |

3.51% |

49.37% |

||

|

Organic farming |

3.80% |

49.16% |

1.83% |

1.83% |

14.85% |

24.86% |

3.67% |

49.46% |

||

| 184

Plums |

Conventional farming |

47.24% |

2.22% |

27.84% |

4.12% |

4.84% |

13.07% |

51.41% |

||

|

Organic farming |

52.00% |

2.49% |

19.97% |

1.66% |

10.71% |

2.65% |

10.52% |

58.75% |

||

|

Cherries |

Conventional farming |

1.95% |

14.57% |

12.33% |

2.27% |

21.28% |

39.21% |

8.33% |

60.78% |

|

|

Organic farming |

7.39% |

27.78% |

6.98% |

2.01% |

22.20% |

26.79% |

6.85% |

53.05% |

||

|

Kiwis |

Conventional farming |

54.10% |

4.80% |

21.05% |

9.89% |

8.18% |

44.16% |

|||

|

Organic farming |

34.59% |

8.68% |

9.43% |

4.04% |

5.05% |

25.53% |

12.68% |

50.08% |

||

|

Table grapes |

Conventional farming |

2.96% |

11.02% |

30.08% |

53.08% |

66.43% |

||||

|

Organic farming |

5.16% |

19.28% |

21.34% |

48.41% |

3.34% |

2.47% |

54.61% |

|||

Source: Orchard Survey (2012)

185Tab. 6 – Econometric models.

|

Apples |

Apricots |

Pears |

Peaches |

Plums |

Cherries |

Kiwis |

Table grapes |

All fruits |

|

|

Marketing channels |

|||||||||

|

Direct selling |

0.2808*** |

0.2489 |

1.0836*** |

0.4312 |

1.4338*** |

0.9798*** |

0.8447*** |

1.1331*** |

1.0462*** |

|

Indirect selling |

0.1822** |

0.4620 |

0.0622 |

0.8558** |

0.6619 |

0.9632*** |

0.7999** |

0.9347*** |

0.5994*** |

|

Identified long channel |

0.3898*** |

1.7827*** |

0.5805*** |

2.1823*** |

-1.4139 |

1.6895*** |

1.0529* |

0.4816* |

0.9157*** |

|

Unidentified long channel |

-0.2180*** |

0.2904 |

-0.2994 |

0.9814** |

-0.1008 |

0.4213* |

0.1782 |

0.2496 |

0.3983*** |

|

Farm status |

|||||||||

|

Individual farm |

0.1670 |

0.6763*** |

0.0606 |

0.1462 |

-0.2635 |

0.4783 |

0.0817 |

0.8606*** |

0.2945*** |

|

Farm location (reference: Other regions) |

|||||||||

|

Aquitaine |

0.0198 |

-1.9539 |

0.4935 |

0.8707 |

-1.0460*** |

-1.8593 |

0.5042 |

-0.4652 |

-0.0541 |

|

Languedoc-Roussillon |

0.0715 |

-1.1918 |

-0.3202 |

0.2658 |

-0.7996 |

-1.1179 |

0.0201 |

-0.4511 |

-0.3177** |

|

Limousin |

-0.2598 |

13.8687 |

13.5240 |

10.3376 |

8.9516 |

0.6975** |

|||

|

Midi-Pyrénées |

0.0981 |

-0.3343 |

0.9432 |

2.1722* |

-0.4405 |

0.0801 |

0.8593* |

0.2131 |

0.0234 |

| 186

Centre-Val de Loire |

0.0291 |

-0.4333 |

-1.2692 |

-1.0639 |

-0.2735 |

-0.7223 |

9.9362 |

-0.0948 |

|

|

Provence-Alpes-Côte d’Azur |

0.0363 |

-0.9039 |

-0.6788** |

0.6407 |

-1.6919*** |

-0.5509 |

-1.0342 |

0.00874 |

-0.1014 |

|

Rhone-Alpes |

-0.1518* |

-0.1643 |

0.0602 |

0.8982 |

0.0524 |

0.00379 |

-0.6655* |

-0.7392 |

0.4459*** |

|

Other control variables |

|||||||||

|

Acreage |

0.0000 |

0.0003*** |

0.0000 |

0.0001 |

0.0000 |

0.0000 |

0.0001** |

0.0002** |

0.0001 |

|

Acreage2 |

0.0000 |

-0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

-0.0000 |

-0.0000 |

_0.0000 |

|

Intercept |

2.0038*** |

2.8713** |

3.0111*** |

3.3650*** |

3.9136*** |

4.1279*** |

1.8774*** |

2.2442*** |

3.1852*** |

|

Concordance rate |

68.9% |

73.7% |

66.4% |

72.9% |

64.5% |

72.6% |

73.0% |

68.6% |

74.1% |

|

Number of observations |

3,821 |

2,244 |

1,634 |

1,346 |

2,355 |

3,269 |

873 |

1,657 |

14,334 |

Keys: Estimates significant at the 10 % (*), 5 % (**) and 1 % (***) thresholds.

Source: Orchard Survey (2012).

187To go beyond this analysis, an econometric model is implemented which confirms the results presented above (Table 6). Whatever the fruit considered, econometric results confirm that some marketing channels, not only short ones, are more likely to go hand in hand with organic farming certification.

Short food supply chains, defined both in terms of direct and indirect selling, influence positively and consistently the adoption of organic farming certification for fruits in general and most major fruit types in particular. Moreover, most coefficients are very significant (1% level). This result contrasts with long food supply chains whose coefficients are less significant and even sometimes negative (H1 validated). It is in line with previous observations made in the literature on the close link between short food supply chains and organic farming.

Similarly, within each type of food supply chain, there are marked differences. For example, direct selling favors more organic farming than indirect selling (H2 validated), and the same is true for long identified circuits compared to long non-identified circuits (H3 validated). This result can be noticed for both the value and the significance of the coefficients for all types of fruits, with some rare exceptions (peaches for short food supply chains).

More interestingly, direct selling and identified long channels are the most likely to encourage organic production. The predominance of one of these two types of marketing channels appears to vary greatly from one production to another. Identified long channels have the biggest positive influence on the production of organic apples, apricots, peaches, cherries and kiwis, while direct selling is the main driver for the production of organic pears, plums, table grapes and all fruits in general. Beyond the differences between fruits, this result reflects the fact that when a farmer knows the destination of his produce, he is more involved in the quality of the produce and more likely to adopt more environmentally-friendly practices.

This result has to be put into perspective with the collective policy of producer organizations (POs). The aim of these organizations is to match supply and demand, by assigning and allocating specific markets to producers (Silva et al., 2014). Because one single producer cannot meet the total suppliers’ requirements, POs allow producers to meet the supply needs collectively. Conversely, a farmer who sells all or part 188of his production to POs is not necessarily likely to adopt this certification even if the organic certification is requested by some suppliers.

The results also confirm that the status of the farm has an impact on the adoption of organic farming certification, especially for apricots and table grapes. For these products, farmers are more likely to implement more environmentally-friendly practices since their farms operate on an individual basis (H4 validated). We also notice that these farmers benefit from a larger acreage (H5 not validated). This might be explained by the perishability and associated production and marketing risk of these specific products.

The results also show that, for the most part, location has no specific influence on the adoption of organic farming (H6 not validated). A few regions are more commonly associated with organic farming, such as Limousin and Rhône-Alpes. Similarly, few differences exist between fruit specializations (H7 validated). This result is salient regarding the influence of the marketing channel, which is consistent for short food supply chains and for identified long channels. They indicate that fruit producers display similar behavior at the national scale, whatever their production. Such a result may emphasize the influence of public policies on the adoption of organic farming.

Conclusion

In this article, we have endeavored to analyze the link between the choice of marketing channel and the adoption of organic farming. The existing literature emphasized a strong link between these two main aspects of farm production processes. The question is important for fruit production, a sector which is an intensive consumer of phytosanitary products and which is prone to the adoption of alternative supply chains.

This study focused on French fruit-producing farms, considering both overall fruit production and the different types of fruit produce. Data was taken from the 2012 ‘Orchard Survey’, a census representative of French farms that provides a detailed overview of marketing channels and phytosanitary practices, as well as key indicators of the farm structure.

189The originality of the study is first, to go beyond the traditional dichotomy between short food and long food supply chains and second, to consider the diversity of channels. The results were twofold. First, they confirmed the existence of a strong and positive relationship between short food supply chains and organic farming, these two strategies being oriented toward increased produce quality. Second, they highlighted that some long channels were also associated with the development of organic farming when the destination of the product is known. A relative transparency of the supply chain is therefore a key criterion that favors the adoption of organic practices.

These results proved the importance of marketing channels in the adoption of new production chains, oriented towards quality and environmentally-friendly practices. It would be interesting to extend the analysis to more recent years given that the Orchard Survey was not reedited yet. Considering other crops, and more precisely annual ones, would also provide additional knowledge. Because most farmers are able to combine marketing channels, an analysis of the interaction between them would also be relevant. Such an analysis would allow us to enjoy a more precise understanding of farmers’ choices relating to marketing channels by linking them to the suppliers’ phytosanitary requirements. In terms of public policies, a more in-depth knowledge of marketing strategies suitable for organic farming may improve the way by which farms are able to adopt new production strategies.

190References

Agence Bio, 2020, Chiffres clés 2019, http://www.agencebio.org, Accessed January 26, 2021.

Akerlof G.A., 1970, “The market of ‘lemons’: quality uncertainty and the market mechanism”, Quarterly Journal of Economics, vol. LXXXIV, p. 488-500.

Asian A., Hafezalkotob A., Jubin J.J., 2019, “Sharing economy in organic food supply chains: A pathway to sustainable development”, International Journal of Production Economics, vol. 218, p. 322-338.

Aubert M., Enjolras G., 2014, “The determinants of input use in agriculture: A dynamic analysis of the wine-growing sector in France”, Journal of Wine Economics, vol. 9, no 1, p. 75-99.

Aubert M., Enjolras G., 2016, “Do short food supply chains go hand in hand with environment-friendly practices? An analysis of French farms”, International Journal of Agricultural Resources, Governance and Ecology, vol. 12, no 2, p. 189-213.

Aubert M., Enjolras G., 2017, “French labour-force participation in organic farming”, Human Systems Management, vol. 36, no 2, p. 163-172.

Barham B., Foltz J., Jackson-Smith D., Moon S., 2004, “The dynamics of agricultural biotechnology adoption: lessons from rBST use in Wisconsin, 1994-2001”, American Journal of Agricultural Economics, vol. 86, p. 61-72.

Barry C., 2012, « Un producteur sur cinq vend en circuit court », Agreste Primeur, vol. 276.

Broderick S., Wright V., Kristiansen P., 2011, “Cross-Case Analysis of Producer-Driven Marketing Channels in Australia”, British Food Journal, vol. 113, no 10, p. 1217-1228.

Buck D., Getz C., Guthma J., 1997, “From farm to table: The organic vegetable commodity chain of Northern California”, Sociologia Ruralis, vol. 37, no 1, p. 3-20.

Burton M., Rigby D., Young T., 2003, “Modelling the adoption of organic horticultural technology in the UK using duration analysis”, The Australian Journal of Agricultural and Resource Economics, vol. 47 No.1, p. 29-54.

Butault J.-P., Dedryver C.-A., Gary C., Guichard L., Jacquet F., Meynard J.-M., Nicot P., Pitrat M., Reau R., Sauphanor B., Savini I., Volay T., 2010, Ecophyto R&D, quelles voies pour réduire l’usage des pesticides, INRA, Paris.

Camanzi L., Malorgio G., García Azcárate T., 2011, “The Role of Producer Organizations in Supply Concentration and Marketing: A Comparison between European Countries in the Fruit and Vegetable Sector”, Journal of Food Products Marketing, vol. 17, no 2-3, p. 327-354.

191Cavaliere A., Peri M., Banterle A., 2016, “Vertical Coordination in Organic Food Chains: A Survey Based Analysis in France, Italy and Spain”, Sustainability, vol. 8, no 6, p. 1-12.

Chiffoleau Y., Dourian T., 2020, “Sustainable Food Supply Chains: Is Shortening the Answer? A Literature Review for a Research and Innovation Agenda”, Sustainability, vol. 12,, no 23, 9831.

Coppola, A., Ianuario, S., 2017, “Environmental and social sustainability in Producer Organizations’ strategies”, British Food Journal, vol. 119, no 8, p. 1732-1747.

Costa S., Zepeda L., Sirieix L., 2014), “Exploring the social value of organic food: A qualitative study in France”, International Journal of Consumer Studies, vol. 38, no 3, p. 228-237.

Darnhofer I., Schneeberger W., Freyer B., 2005, “Converting or not converting to organic farming in Austria: Farmer types and their rationale”, Agriculture and Human Values, vol. 22, p. 39-52.

Diederen P., van Meijl H., Wolters A., Bijak K., 2003, “Innovation adoption in agriculture: Innovators, early adopters and laggards”, Cahiers d’Économie et de Sociologie Rurales, vol. 67, p. 29-50.

Dubuisson-Quellier S., Navarrete M., Pluvinage J., 2006, « Les organisations de producteurs au cœur de la valorisation de la qualité des fruits. Une diversité de stratégies en Rhône-Alpes », Économie Rurale, vol. 292, p. 19-34.

European Commission, 2018, “The contribution of producer organizations to an efficient agri-food supply chain”, Brussels, 11 p.

Fernandez-Cornejo J., 1996, “The microeconomic impact of IPM adoption: Theory and application”, Agricultural and Resources Economics Review, vol. 25, no 2, p. 149-160.

Fernandez-Cornejo J., Ferraioli J., 1999, “The environmental effects of adopting IPM techniques: The case of peach producers”, Journal of Agricultural and Applied Economics, vol. 31, no 3, p. 551-564.

France - French Ministry of Agriculture, 2012, « Un producteur sur cinq vend en circuit court », Agreste Primeur, 275.

Galli F., Bartolini F., Brunori G., Colombo L., Gava O., Grando S., Marescotti A., 2015, “Sustainability assessment of food supply chains: an application to local and global bread in Italy”, Agricultural Economics, vol. 3, no 21, 21.

Galt R.E., 2008, “Toward an Integrated understanding of pesticide use Intensity in Costa Rican vegetable farming”, Human Ecology, vol. 36, no 5, p. 655-677.

Giraud-Héraud E., Rouached L., Soler L.-G., 2006, “Private labels and public quality standards: How can consumer trust be restored after the mad cow crisis?”, Quantitative Marketing and Economics, vol. 4, no 1, p. 31-55.

192Hardesty S.D., Leff P., 2010, “Determining marketing costs and returns in alternative marketing channels”, Renewable Agriculture and Food Systems, vol. 25, p. 24-34.

Hazell P., Poulton C., Wiggins S., Dorward A., 2010, “The future of small farms: trajectories and policy priorities”, World Development, vol. 38, no 10, p. 1349-1361.

Heckman J., 2006, “A history of organic farming: Transitions from Sir Albert Howard’s War in the Soil to USDA National Organic Program. Renewable Agriculture and Food Systems”, vol. 21, no 3, p. 143-150.

Hwang J., Chung J.-E., 2019, “What drives consumers to certain retailers for organic food purchase: The role of fit for consumers’ retail store preference”, Journal of Retailing and Consumer Services, vol. 47, p. 293-306.

Ilbery B., Kirwan J., Maye D., 2014, “Explaining regional and local differences in organic farming in England and Wales: A comparison of South West Wales and South East England”, Regional Studies, vol. 50, p. 110-123.

Kottila M.R., Rönni P., 2008, “Collaboration and trust in two organic food chains”, British Food Journal, vol. 110, no 4/5, p. 376-394.

Lamine C., 2011, “Transition pathways towards a robust ecologization of agriculture and the need for system redesign. Cases from organic farming and IPM”, Journal of Rural Studies, vol. 27, p. 209-219.

Läpple D., van Rensburg T., 2011, “Adoption or organic farming: Are there differences between early and late adoption?”, Ecological Economics, vol. 70, p. 1406-1414.

Lee T.H., Fu C.-J., Chen Y.Y., 2020, “Trust factors for organic foods: consumer buying behavior”, British Food Journal, vol. 122, no 2, p. 414-431.

Lind K., Lafer G., Schloffer K., Innerhofer G., Meister H., 2004, Organic fruit growing, CABI Publishing, Wallingford.

Lombardi A., Migliore G., Verneau F., Schifani G., Cembalo L., 2015, “Are ‘good guys’ more likely to participate in local agriculture?” Food Quality and Preference, vol. 45, p. 158-165.

Łuczka W., Kalinowski S., 2020, “Barriers to the Development of Organic Farming: A Polish Case Study”, Agriculture, vol. 10,, no 11, 536.

McNamara M.E.W., Keith Douce G., 1991, “Factors affecting peanut producer adoption of integrated pest management”, Review of Agricultural Economics, vol. 13, no 1, p. 129-139.

Maréchal G., Spanu A., 2010, « Les circuits courts favorisent-ils l’adoption de pratiques agricoles plus respectueuses de l’environnement? » Courrier de l’environnement de l’INRA, vol. 59, p. 33-45.

Martinez S., Hand M., Da Pra M., Pollack S., Ralston K., Smith T., Vogel S., Clark S., Lohr L., Low S., Newman C., 2010, Local Food Systems: Concepts, Impacts, and Issues, ERS Report Summary, U.S. Department of Agriculture.

193Michalek J., Ciaian P., Pokrivcak J., 2018, “The impact of producer organizations on farm performance: The case study of large farms from Slovakia”, Food Policy, vol. 75, p. 80-92.

Michel S., 2014, « La survie des intermédiaires face au circuit court: le cas des grossistes en fruits et légumes », Management & Avenir, vol. 71, p. 135-152.

Michelsen J., 2001, “Organic farming in a regulatory perspective: The Danish case”, Sociologia Ruralis, vol. 41, no 1, p. 62-84.

Moati P., Ranvier M., 2005, « Faut-il avoir peur du hard-discount? », Consommation et Modes de Vie, Credoc, 188.

Moustier P., Nguyen T.T.L., 2013, « Le circuit court, mode de certification sanitaire des légumes au Vietnam », INRA-SFER-CIRAD Conference, 12-13 December 2013, Angers, France.

Penker M., 2006, “Mapping and measuring the ecological embeddedness of food supply chains”, Geoforum, vol. 37, no 3, p. 368-379.

Renting H., Marsden T., Banks J., 2003, “Understanding alternative food networks: Exploring the role of short food supply chains in rural development”, Environment and Planning A, vol. 35, no 3, p. 393-411.

Richards T.J., Acharya R.N., Molina I., 2011, “Retail and wholesale market power in organic apples”, Agribusiness, vol. 27, no 1, p. 62-81.

Ritchie R., Brindley C., 2000, “Disintermediation, disintegration and risk in the SME global supply chain”, Management Decision, vol. 38, no 8, p. 575-583.

Rouvière E., Latouche K., 2014, “Impact of liability rules on modes of coordination for food safety in supply chains”, European Journal of Law Economics, vol. 37, no 1, p. 111-130.

Scandella D., Christy G., 2011, « L’approvisionnement des magasins en circuit court: opportunités et menaces pour la filière fruits et légumes », Infos Ctifl, vol. 271, p. 18-25.

Smith A., 2006, “Green Niches in Sustainable Development: The Case of Organic Food in the United Kingdom”, Environment and Planning C: Government and Policy, vol. 24, no 3, p. 439-458.

Souza Monteiro D.M., Caswell J.A., 2009, “Traceability adoption at the farm level: An empirical analysis of the Portuguse pear industry”, Food Policy, vol. 34, no 1, p. 94-101.

Silva A.C.G.C., Barbosa A.S., Fontes C.H., 2014, “Certification rules for the fruit agri-business”, African Journal of Agricultural Research, vol. 9, no 37, p. 2805-2813.

Steffen A., Doppler S., 2019, “Building consumer trust and satisfaction through sustainable business practices with organic supermarkets: The case of Alnatura”, in Byrom, J., Medway D., Eds., Case Studies in Food Retailing and Distribution, Elsevier, United Kingdom, p. 205-228.

194Sylvander B., Schieb-Bienfait N., 2006, “The strategic turn of Organic Farming in Europe: From a resource based to an entrepreneurial approach of Organic Marketing Initiatives”, in Marsden T., Murdoch J., Eds., Between the local and the global, Confronting complexity in the contemporary food sector, Emerald Group Publishing Limited, Oxford, p. 323-358.

Taghikhah F., Voinov A., Shukla N., 2019, “Extending the supply chain to address sustainability”, Journal of Cleaner Production, vol. 229, p. 652-666.

Tundys B., Wiśniewski T., 2020, “Benefit Optimization of Short Food Supply Chains for Organic Products: A Simulation-Based Approach”, Applied Sciences, vol. 10, no 8, 2783.

Tuomisto H.L., Hodge I.D., Riordan P., Macdonald D.W., 2012, “Does organic farming reduce environmental impacts? A meta-analysis of European research”, Journal of Environmental management, vol. 112, p. 309-320.

Uematsu H., Mishra A.K., 2012, “Organic farmers or conventional farmers: Where’s the money?”, Ecological Economics, vol. 78, p. 55-62.

Venn L., Kneafsey M., Holloway L., Cox R., Dowler E., Tuomainen H., 2006, “Researching European “alternative” food networks: Some methodological considerations”, Area, vol. 38, no 3, p. 248-258.

Weibel F., 2002, “Organic Fruit Production in Europe”, The compact fruit tree, vol. 35, no 3, p. 77-82.

Zhou J., Elen J.H., Liang J., 2011, “Implementation of food safety and quality standards: A case study of vegetable processing industry in Zhejiang, China”, The Social Science Journal, vol. 48, no 3, p. 543-552.