Le statut évolutif de la confiance dans la relation entre les clients vulnérables et les banques Une étude longitudinale

- Type de publication : Article de revue

- Revue : European Review of Service Economics and Management Revue européenne d’économie et management des services

2021 – 1, n° 11. varia - Auteurs : Amine (Abdelmajid), Gatfaoui (Shérazade)

- Pages : 55 à 86

- Revue : Revue Européenne d’Économie et Management des Services

THE EVOLVING STATUS OF TRUST

IN THE RELATIONSHIP BETWEEN VULNERABLE CUSTOMERS AND BANKS

A longitudinal study

Abdelmajid Amine1a

Shérazade Gatfaouia

aIRG – Université Paris Est-Créteil et Université Gustave Eiffel

INTRODUCTION

The latest Ipsos-le Secours Populaire poverty barometer2, which tracks the state of poverty in France, confirms and reinforces the trend towards the impoverishment and precariousness of a large part of the French population, observed since the economic and financial crisis of 2008. The results show, not surprisingly, an explosion of poverty during and after lockdown due to Covid-19, with one respondent in 10 admitting to living in poverty, an increase of 5 points compared to 2019. Feelings of vulnerability and downgrading are increasing compared to previous years and a strong concern for the future of children is taking hold among the vast majority of those surveyed. Nearly 40% of the people surveyed are financially extremely vulnerable, causing major difficulties on a daily basis in terms of food and covering current expenses (residence, energy, 56care). This financial fragility (one French person in three has suffered a loss of income according to this barometer) naturally translates into a tendency for households to become over-indebted, which is a visible expression of their vulnerability. Vulnerability, in this context, has been defined by Gondard-Delcroix and Rousseau (2004, p. 1) as “the likelihood of welfare deterioration as a result of a shock produced by external pressures on dominated individuals.” Today, life incidents (unemployment, illness, death, divorce, etc.) affect all social classes, from the upper classes to young high-school graduates (Couret and Metzger, 2009), and people from these social classes and statuses, who have traditionally been spared, are increasingly experiencing temporary vulnerability (Amine and Gatfaoui, 2019) because they are now in an uncertain environment that can jeopardize their financial security and personal situation at any time.

Nevertheless, research on the concept of vulnerability is still insufficiently developed in the marketing literature and its understanding remains rather relative, despite the development of work in the field of consumption (Brenkert, 1998; Baker et al., 2005; Pavia and Mason, 2014) and more recently in services (Rosenbaum et al., 2011, 2017; Anderson et al., 2013; Anderson and Ostrom, 2015; Johns and Davey, 2019). Indeed, it is a notion that is sometimes “misunderstood” or improperly used (Ringold, 1995; Smith and Cooper-Martin, 1997; Baker et al., 2005). It is sometimes linked to socio-demographic characteristics, sometimes associated with consumer stigmatization or, conversely, with consumer protection, unmet needs, discrimination, or life disadvantages. Baker et al. (2005) addressed this diversity of conceptions and approaches by emphasizing that consumer vulnerability is a multidimensional concept whose understanding is specific to the context in which it is applied (health, poverty, illiteracy, old age, etc.).

If there is one economic sector that represents a singular context in which this vulnerability is expressed, because of its close relationship to money, financing, and consumption, it is the banking sector. However, the study of customer vulnerability in the banking sector is paradoxically underdeveloped in academic marketing research (Wang and Tian, 2014), even though taking into account the situations of vulnerability encountered by bank customers would make it possible both to better understand the issues involved in managing the banking relationship with this fragile population and to identify the levers that promote adjustments to these situations, which have become fairly recurrent.

57The concept of the banking relationship refers to the direct involvement of three stakeholders, namely the client, the advisor, and the banking organization to which the latter is attached, as well as the mobilization of their respective resources to nurture and sustain this relationship. Although this articulation (more or less harmonious) can be established in the context of a so-called “normal” relationship without any significant banking incident, this concept takes a different turn when it concerns a relationship that involves vulnerable clients experiencing episodes of financial fragility. Indeed, the latter type of relationship seems at first sight to place the stakeholders (advisor/organization–vulnerable client) in a highly unbalanced relationship to the benefit of the bank/advisor, who are in position to impose restrictive or constraining conditions on these clients. However, this clear-cut vision would, in our opinion, benefit from being reassessed insofar as it assumes, on the one hand, that the bank has no interest in building trust with these fragile clients and keeping them in its business portfolio and, on the other hand, that vulnerable customers passively suffer this situation and have neither the resources nor the latitude to make their voice heard, defend their interests, or maintain their economic and social inclusion.

A study conducted by Deloitte (2019) shows that, while bank customers are generally satisfied with the services provided by their bank, 35% of respondents said they do not trust their bank. Bank branches continue to play a central role in the relationship that customers have with their bank. A total of 45% of French people prefer to go through their bank branch (reception area or advisor) to carry out complex transactions. This study also highlights that French people expect their bank to support them and trust them during periods in life likely to alter their financial situation. Only 30% of respondents felt they had good support when making a claim, and only 11% of clients said they received sufficient support during their period of unemployment, 18% in the case of the death of a close relative, and 15% in the case of divorce. These statistical cues show that, during episodes of vulnerability, clients feel neither sufficiently supported nor helped by their advisor/bank. Moreover, the recurring scandals in the banking sector and the current economic crisis reinforce the necessity to understand how to build, maintain, or restore trust in order to reassure clients, including vulnerable clients, and build loyalty over the long term. In this context, the need to recreate the bond of trust with customer becomes clear. To respond to this “need 58for trust,” some banks have utilized the motivation of proximity and shared values, as illustrated by the slogan of the Crédit Mutuel Bank (“A bank that belongs to its client-members, that changes everything”), thus underlining the relevance of trust in the banking relationship.

At the heart of this banking relationship is the notion of trust, which underpins its durability and binds together the stakeholders involved within it. Trust is a notion that has provoked considerable interest both from researchers and practitioners in the fields of psychology, sociology, economics, and, more recently, marketing and management. The concept is at the core of numerous studies, in particular with regard to its nature, its status, and how it is built in business relationships. Trust has been defined in marketing literature as putting one’s fate in the hands of others within the course of a (social or merchant) relationship. Mayer et al. (2007, p. 712) proposed the following definition of trust, which is suitable in our context in the sense that it binds this concept to vulnerability: “Trust is the willingness of a party to be vulnerable to the actions of another party based on the expectation that the other will perform a particular action important to the trustor, irrespective of the ability to monitor or control that other party.”

Moreover, if briefly synthesize the theoretical work on trust, it is possible to identify two perspectives in studying this concept. The first approach, a “static” one, attempts to study and measure the concept of trust – its dimensions, antecedents, and consequences – at a particular moment (T) of a relationship. The second approach is more dynamic, but much less developed in management, and aims to ensure a better understanding of the processes by which trust is built over the course of time (Ring and Van de Ven, 1992; Zajac and Olsen, 1993), then strengthened or weakened during the multiple interactions between the partners. This process-based perspective on the evolution of trust has particular relevance in the case of the banking relationship between clients who are going through one or more episodes of vulnerability and their advisor, insofar as these difficulties put the contract of trust between these stakeholders to the test.

In this research we address the following key questions:

1. How is trust built and how does it evolve in vulnerable customer–bank relationships?

2. How do the nature and status of trust change over time?

59Drawing on the literature, the first part of the paper aims to conceptualize trust and underline the relevance of the dynamic perspective to study its development and/or dissolution processes within service relationships with vulnerable clients. We then present the research methodology, based on a qualitative and longitudinal study conducted with dyads of bank advisors and financially fragile customers in the French banking context. To understand how trust is built and evolves in the banking relationship, we analyzed the practices and strategies of both actors in the dyad, composed of clients and their advisors, when the former go through one or more episodes of vulnerability that have generated banking incidents. Finally, the empirical findings are discussed, and the main implications are expounded regarding banking institutions and public policy aiming to improve vulnerable customers’ opportunities for inclusion and to preserve their consumption and well-being.

1. DOES DIFFERENTIATING TRUST AT INSTITUTIONAL

OR INTERPERSONAL LEVELS MATTER?

Trust is a complex, multifaceted concept and, whether it is interpersonal or institutional, it is often recognized as an essential variable in the success of management exchanges, sometimes related to the notion of “calculation” (Williamson, 1993). Trust has been at the heart of many works in management sciences, particularly with regard to its definition and dimensions, in both B2B and B2C relationships (Grönroos, 1990; Morgan and Hunt, 1994; Guibert, 1999).

Some authors have highlighted the different meanings attributed to trust and proposed a multidisciplinary vision of trust within and across organizations (e.g. Rousseau et al., 1998). According to such authors, psychologists equate trust with the personality and behavioral attributes of individuals (Deutsch, 1958), economists consider trust to be the result of a calculation based on the hypotheses of actors’ opportunism and rationality (Williamson, 1993), and sociologists analyze trust through the embedded properties of relations between actors and within institutions or social systems (Granovetter, 1985). These social, psychological, and 60symbolic dimensions of trust attenuate its purely economic status and enrich its interpretation in business relationships. Trust is thus established and built within the framework of social relations, taking into account the personality of the partners, their feelings and experiences, and their culture and ethics as much as their rationality.

To understand the building and development of trust in business relationships, researchers and practitioners have been led to question the nature of relationships (interpersonal versus institutional) in which trust mostly intervenes along the course of encounters between these exchange partners.

1.1. THE PREVALENCE OF THE INTERPERSONAL DIMENSION

OF TRUST IN THE SERVICE RELATIONSHIP

Service marketing initially emphasized the importance and role of interpersonal relationships between front-line staff and the client in the stability of their exchanges (Eiglier and Langeard, 1987; Moorman et al., 1992; Morgan and Hunt, 1994). Early research pointed out the predominant role of the interpersonal dimension in performing the exchange relationship (Mayaux and Flipo, 1995; Lovelock and Lapert, 1999) thus lessening and/or obscuring the contribution of the service-providing firm (institutional level). Such work thus highlighted the essential role of personnel in contact with customers in the efficiency of business relations and the long-term orientation of exchanges between the partners (Berry, 1995), conflict management, or the development of trust-based exchange with customers. This predominance of the interpersonal dimension of the relationship compared to the institutional one in service activities is explained by the very nature of the service involving direct interaction with the provider, although one can witness a decrease in interpersonal interaction between client and staff due to the digital transformation of the relationship.

This prevalence of interpersonal trust in service relationships, as well as the perceived risk linked to the banking and financial sector, lead us to question the status of trust in the relationship between customers and front office staff and its evolution across service encounters. The presumed importance of the interpersonal dimension of trust in the banking relationship seems to be further amplified when dealing with vulnerable clients (or clients going through episodes of vulnerability) 61insofar as these customers turn less to the anonymous, distant, and abstract banking institution than to an advisor who is (more or less) familiar, empathetic, and involved in looking for solutions to the problems encountered by the client. The situation of vulnerability is therefore expected to overvalue the role of interpersonal aspect of trust in the construction, reinforcement, and preservation of the service relationship, compared to the institutional dimension.

1.2. THE INSTITUTIONAL LEVEL OF TRUST

IN THE SERVICE RELATIONSHIP

Some authors have stressed the importance of a broadened conception of the exchange relationship to include the social network (Granovetter, 1985; Grönroos, 1990) of the actors, which involves the organization and the market in addition to the interpersonal interactions between the customer and the salesperson. Thus, the service relationship between vendors and customers can be integrated into a more global relationship between the firm and the consumers (Bergadaa et al., 1999; Besson and Gurviez, 2000) that can potentially increase trust between the parties. Whether at the interpersonal or institutional level of the relationship, research has highlighted the crucial role of trust in sustaining exchanges and strengthening the relationship (Morgan and Hunt, 1994; Doney and Cannon, 1997). Taking these two levels of the relationship into account allows trust with the client to be built and better maintained over time. In the current context of uncertainty characterized by a growing risk of consumer vulnerability and the inclination of bank staff to mobility in the job market, it seems appropriate for the organization to prioritize the institutional aspect of trust, which is more durable and less risky than the interpersonal dimension insofar as the staff in contact (particularly in the French banking sector) undergoes a high turnover, which introduces a degree of randomness into the sustainability of the relationship if it is primarily built on interpersonal trust. To do so, banks might emphasize corporate communication to create a feeling of proximity with their clientele, to be perceived as reliable by their targeted consumers, and to emphasize their values of benevolence and efficiency.

621.3. THE RELEVANCE OF A LONGITUDINAL APPROACH

TO STUDY TRUST IN VULNERABLE CLIENT–ADVISOR RELATIONSHIPS

The literature identifies two approaches to study trust in exchange relationships: a static one, dominant in management research, which captures trust as a state that can be located/situated and measured at a given time; and a dynamic approach, much less developed, which conceives trust as being built as a process, continuously strengthened (or weakened) over time. Relatively recent research has highlighted the lack of empirical work related to understanding the processes of trust development in business relationships (Mayer et al., 2007; Huang and Wilkinson, 2013; Schilke and Cook, 2013). Our research is in line with this perspective and aims to contribute to filling this gap through a longitudinal study of trust in the less explored case of the vulnerable customer–bank advisor relationship.

In the marketing literature, trust is indiscriminately defined as a belief, expectation, feeling, behavioral intention, or willingness to rely on an exchange partner within perceived risky situations (Moorman et al., 1992; Chaudhuri and Holbrook, 2001). Some authors consider trust as a concept referring both to the credibility and the benevolence of the exchange partner (Doney and Canon, 1997; Ganesan, 1994; Morgan and Hunt, 1994), to which other authors add honesty (Hess, 1995). The definitions provided, however, do not explicitly address the dynamic nature of trust as embodied in a cycle of development as it is tested through the service experiences (positive or negative) shared by partners. Prior studies have mainly aimed to define and measure trust at a given time, while ignoring the construction process of trust that stems from a longitudinal perspective (Dwyer et al., 1987; Zajac and Olsen, 1993; Ring and Van de Ven, 1994).

The literature review also reveals various determinants and consequences of trust according to its application contexts, namely industry, services, retailing, and bank-to-bank or bank-to-customer relationships (Andaleeb, 1991; Geyskens and Steenkamp, 1995; Moorman et al., 1992). However, some variables, such as satisfaction, cooperation, and communication, appear either as antecedents or consequences of trust. Thus, analyzed from a static view of trust, these determinants and consequences hide the time dimension, which may exhibit the stage of development of the relationship being studied. One can hypothesize 63that a dynamic approach to trust may reconcile the former conflicting findings in the literature about the double status of these variables (being considered both as antecedents and consequences) that emerge in the static approach. This shift in the conception of trust must be accompanied by a change in the method used to observe and analyze this construct, which may contribute to a better understanding of the mechanisms underlying trust building.

This research avenue is all the more interesting since it seems relevant to study the banking relationship with vulnerable customers, who are experiencing unplanned incidents that may change the development of their trust in the advisor and the bank as a whole.

2. METHODOLOGY

To understand how trust is built and evolves in the relationship between vulnerable clients and their bank advisors, we analyzed the practices of a mutual bank, BRED3 Banques Populaires, through a qualitative and longitudinal research based on 18 retrospective interviews carried out with clients who had experienced fairly serious banking incidents within the last three years. This made it possible to capture and analyze the discourses of customers around their service encounters and the management of incidents that occurred during their relationship. The critical incident method enables the identification of negative events that arise between clients and their bank advisors, as well as the way they are handled, and allow a clearer understanding of the development process of trust and the mechanisms by which it is built. Finally, the dynamic approach allows the historical relationship to be retraced from the perspective of these fragile customers.

In-depth interviews were conducted with vulnerable customers, enriched with the critical incident method (Flanagan, 1954; Bitner et al., 1990; Keaveney, 1995), which made it possible to take into account the episodes of vulnerability encountered by customers when retracing their banking relationship history. Thus, their narratives were built around 64negative events (or incidents) that had occurred over the last three years and their management by the bank. These incidents perform the role of a memory milestone, allowing a narrative based on these events to be created, making the discourse more reliable. These incidents can be caused by the client (due to deviant behavior such as compulsiveness, over-consumption in times of resource restriction, etc.), by external factors (illness, job loss, reduced income, divorce) that hinder the client’s financial situation, or by the bank through relationship management mistakes (e.g. errors in transferring funds, “forced” sale of an unsuitable financial product or service, etc.).

2.1. DATA COLLECTION

The study was conducted with customers of three bank branches of the BRED Banques Populaires in the Paris region (East, West, Hauts de Seine), who had experienced banking incidents over the last three years. Customers were selected on the basis of three main criteria expounded in the literature: product and services portfolio; duration of the relationship with the bank; and the occurrence of incidents during the customer–bank relationship (in the last three years). Customers needed to have sufficient experience of bank services to be able to discuss trust, and to have been in the advisor’s customer portfolio for at least one year. Bank advisors were also required to have dealt at least once with negative events (either incidents generated by the customer or critical incidents provoked by the bank) in the course of their relationship with the customer.

The targeted clients were identified in collaboration with the branch managers and then contacted by the advisors to explain the purpose of our research (and reveal our academic status) and then arrange an appointment for the interview if they agreed. Given the sensitivity of the subject, several clients contacted declined the invitation to participate in the study. The sample was grown incrementally as data were collected and analyzed. Ultimately, 18 clients aged between 28 to 69 years old met the selection criteria and agreed to be interviewed. Retrospective in-depth interviews were set up one to one, and allowed to retrace each customer’s bank relationship history. Interviewees’ profiles and characteristics of their relationship with the bank are provided in Table 1.

65Tab. 1 – Interviewees’ profiles and characteristics of their relationship with the bank.

|

Age of customer (years) |

Duration of the relationship with BRED bank (years) |

Duration of the relationship with the current advisor (years) |

Context of entry into the relationship with the BRED banka |

Attribution of incidents encountered during the last three years in the relationship with the BRED bank |

|

|

Client no 1 |

29 |

1.5 |

1.5 |

Without prior incident |

Caused by the BRED bank |

|

Client no 2 |

55 |

6 |

1 |

Incidents caused by the client and the former bank and mishandled by the latter |

Caused by the client and the BRED bank |

|

Client no 3 |

42 |

5 |

2 |

Incidents caused by the customer and mismanaged by the former bank |

Caused by the client and the BRED bank |

|

Client no 4 |

33 |

15 |

2 |

Without prior incident |

Caused by the BRED bank |

|

Client no 5 |

45 |

10 |

5 |

Incidents caused by the client and mishandled by the former bank |

Caused by the client and the BRED bank |

|

Client no 6 |

28 |

2 |

2 |

Without prior incident |

Caused by the client and the BRED bank |

|

Client no 7 |

45 |

11 |

2.5 |

Incidents caused by the customer and poorly managed by the former bank |

Caused by the client and the BRED bank |

|

Client no 8 |

61 |

15 |

2.5 |

Without prior incident |

Caused by the BRED bank |

| 66

Client no 9 |

69 |

22 |

2.5 |

Incidents caused by the former bank and mishandled |

Caused by the client and the BRED bank |

|

Client no 10 |

55 |

21 |

1.5 |

Incidents caused by the former bank and mishandled |

Caused by the BRED bank |

|

Client no 11 |

30 |

2.5 |

2.5 |

Incidents caused by the customer and poorly managed by the former bank |

Caused by the customer |

|

Client no 12 |

40 |

23 |

5 |

Incidents caused by the former bank and mismanaged |

Caused by the client and the BRED bank |

|

Client no 13 |

36 |

10 |

3.5 |

Incidents caused by the former bank and poorly handled |

Caused by the BRED bank |

|

Client no 14 |

29 |

10 |

1 |

Without prior incident |

Caused by the BRED bank |

|

Client no 15 |

31 |

12 |

2,5 |

Incidents caused by the customer and poorly managed by the former bank |

Caused by the client |

|

Client no 16 |

63 |

25 |

5 |

Without prior incident |

Caused by the BRED bank |

|

Client no 17 |

57 |

8 |

4,5 |

Incidents caused by the client and mishandled by the former bank |

Caused by the client and the BRED bank |

|

Client no 18 |

51 |

20 |

5 |

Without prior incident |

Caused by the BRED bank |

Note: a This context indicates whether the customer left his/her former bank as a result of incidents (caused by the customer and/or the bank) that were not properly managed.

67These interviews with the selected customers lasted 1 hour and 15 minutes on average and took place at their home or in a café. The interviews were recorded, transcribed, and analyzed. The interview guide was structured around the context of the initial contact with the BRED bank and the client’s expectations and attitudes towards the bank and the advisor at the beginning of the relationship. They were then invited to describe their relationship with the bank and with the current advisor and to talk about the main incidents that have shaped this relationship, the management of these negative events by the actors involved (client/advisor/bank), the results achieved, and the consequences of these negative experiences on the banking relationship. The data collected were then submitted to a thematic content analysis.

3. FINDINGS

As a preliminary analysis, we identified how trust is built up during the banking relationship. We thus highlight three stages through which the construction and testing of trust passes during this relationship: stage 1 (period prior to entering into a relationship with the BRED bank); stage 2 (period relating to the first service experiences with the advisor, facilitating the testing of trust); and stage 3 (subsequent period corresponding to interactions with the advisor following the occurrence of banking incidents as a result of repeated service experiences).

3.1. BUILDING TRUST BEFORE ENTERING

INTO THE RELATIONSHIP WITH THE BANK (STAGE 1)

Before beginning a relationship with any bank, clients mainly consider institutional trust to legitimate the choice. This is quite obvious insofar as the client has not yet experienced the face-to-face relationship with the advisor. At this stage, trust is mainly the result of a cognitive process based on knowledge about the bank as an institution through communication channels (press, TV, Internet, social networks, radio) and word of mouth (WOM) information (through family and friends) 68that gives rise to the feeling that one can rely on and trust a particular bank. Hence, institutional trust relies on the bank’s image, reputation, and perceived expertise, which are reflected in respondents’ statements such as:

“Managing money is their job … BRED Banques Populaires is competitive and close to its customers. It offers a range of services tailored to civil servants … at BRED, you are a member … these are guarantees of trust … my friends have told me that at BRED, they are competent advisors.”

For clients who are in a vulnerable situation at the time of entering into a relationship with the bank, trust can be expressed as an expectation of benevolence from the future bank (and the advisor), backed up by recommendation by relatives for its values of proximity and the human dimension:

“When I asked for an appointment at BRED to request the purchase of 2 COFIDIS loans that were very expensive and which put me in financial difficulty at a time when I had changed job with a lower salary than before, I really expected benevolence from that bank because … when my friend told me about BRED, I had the feeling that I was dealing with a humane bank that trusts its clients … when you are in financial difficulty and you apply for a new bank, you are really in the emotional phase … it almost touches on the intimate side, it is our private life that we have to lay out on the table, so yes, we expect kindness in return because it is not easy to surrender like that … with the fear of judgment.”

This first stage of trust associated with the bank is not only limited to credibility in terms of service quality and security of the funds invested. Clients also underline the affective dimension of the relationship with the bank and with the advisors, which is embedded in the advertisements or WOM:

“They [the Bred Bank] seem nice in the advertisements, it made me want to open an account there and then it’s a cooperative bank … I have the feeling that we can trust … my friend who has an account in this bank told me that they were closer to the clients than in other banks”.

These warning signals contribute to the emergence of a presumption of trust, a feeling that has yet to be confirmed during the first service experiences.

693.2 BUILDING INTERPERSONAL AND INSTITUTIONAL TRUST

DURING THE FIRST SERVICE EXPERIENCES (STAGE 2)

The role played by the first service experiences between customers and advisors is essential in building interpersonal and strengthening institutional trust insofar as they constitute moments of truth (stage 2) allowing the presumption of trust prior to entering into the relationship to be tested.

The first service encounters with the bank advisors allow the identification of the factors contributing to the building of trust and to the shaping of customers’ perceptions of the relationship. When these initial interactions are judged positive (good customer relationship management: “I was really well received … the advisor took time over a cup of coffee … he was able to listen to my problems and provide me with appropriate answers”), the “nascent” interpersonal trust confirms or reinforces the client’s initial institutional trust in the bank. If institutional trust is weakened, interpersonal trust becomes difficult to establish and the banking relationship as a whole is called into question (poor management of the client relationship: “when the advisor is not able to welcome you properly … I don’t see how I can trust this bank”).

Interpersonal trust can be based both on the advisor’s perceived credibility and technical skills, and on the affect, sympathy, and attachment that emerges from the first client–advisor interactions (emotional relationship linked to the fact that the bank advisor knows the history of the relationship with the client, understands the client’s situation of vulnerability, and proposes an adapted and benevolent solution potentially subverting or circumventing the usual procedures). Institutional trust is backed by the bank’s expertise and credibility through the recognized skills of the advisors and the bank’s communication. The affective dimension of institutional trust that can translate into an attachment to the bank brand requires more time to build and is nurtured by the client–advisor experiences over time that affect the image of the bank as an organization.

3.3. TESTING TRUST DURING CLIENT VULNERABILITY EPISODES (STAGE 3)

The status of trust changes as the relationship between the exchange partners evolves. From the status of presumption before entering into the 70relationship to that of a feeling following the first (positive) interactions with the staff and the organization’s services, trust takes the form of a belief when the first banking incident (i.e. an episode of vulnerability experienced by the client) occurs and is well managed by the bank advisor. This last step tests the client’s trust in his/her advisor and in the bank based on how the banking incident is handled and the benevolence expressed toward the client’s situation so that her/his interests are not necessarily harmed to the benefit of the bank.

During repeated service experiences with the bank that led to the management of incidents encountered by these fragile customers (stage 3), the analyses of clients’ discourses show the coexistence of interpersonal and institutional trust. The latter seems to be based both on the credibility of the bank (cognitive dimension of trust) and the feeling that the client can rely on the bank and on its inclination to find solutions that do not harm his/her interests in the event of financial difficulties arising (affective dimension of trust):

“Today, I know that BRED was able to listen to my needs when I was having problems, they accepted to buy back my consumer loans when I was in financial difficulty … that’s when you see the mutualist side, and that you can have confidence in BRED bank … that’s why I like my bank, it is important to me.”

3.4 EXPLORING HOW TRUST IS BUILT AND EVOLVES

DURING THE RELATIONSHIP WITH THE BANK

The content analysis highlights the mechanisms underlying customers’ trust building and development. Initially, we reveal a recursive functioning mode for the interpersonal trust-building process (see section 3.4.1). This kind of trust appears as the major dimension of clients’ reliance in the relationship with the bank. We then propose two modes of interpersonal trust construction, depending on the history of the banking relationship and how incidents have been managed by the advisor from the client’s perspective (see section 3.4.2). Finally, we show some transfer mechanisms from institutional trust to interpersonal trust in the course of the relationship between the customer and the bank/advisor (see section 3.4.3).

713.4.1. Recursive process of interpersonal trust building

Our research shows how some variables are categorized in the literature either as antecedents or consequences of trust. By introducing the time dimension in our analysis, we are able to explain the double status (antecedent and consequence of trust) of certain variables, such as satisfaction, communication, and coordination, depending on the stage of development of the relationship in which the investigation occurs. The construction process of interpersonal trust then takes a recursive form.

For instance, if a customer is satisfied with an initial experience at T period (satisfaction acts as an antecedent), her/his satisfaction may generate trust in the advisor and in the bank, which in turn may reinforce his/her satisfaction (becoming a consequence) in the next encounter (at T+1) (antecedent → consequence → antecedent …). The following quotation illustrates this recursive process of interpersonal trust building:

“Because I am satisfied with my past experience with my advisor, it is easier to have confidence in his proposals. And when things go well, I am satisfied and pleased, and I rely on him now and for the future.”

The communication between customers and bank advisors and the coordination of their behaviors and decisions seem also to contribute to building and reinforcing interpersonal trust, and are in turn improved by it.

These findings show that when we analyze the behaviors and experiences of customers and bank advisors from a longitudinal perspective, we better understand the mechanisms and modes of interpersonal trust building. These findings also corroborate the results of past studies (Andaleeb, 1991; Geyskens and Steenkamp, 1995) that have stressed that good levels of satisfaction and a fluid and continuous communication between the partners strengthen the tendency toward mutual trust.

3.4.2. Modes of interpersonal trust building

The content analysis highlights two ways to build and develop interpersonal trust, depending on the history of the relationship between vulnerable customers and bank advisors, the nature and recurrence of incidents, and how these are handled by the bank.

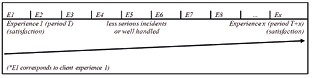

72The first way of building interpersonal trust takes a linear form (Figure 1). This occurs when customers, in their relationship with the bank, are faced with “minor” incidents caused by themselves or with incidents due to mistakes made by the bank management that have been rapidly and favorably resolved by the advisor. In these cases, both customers and advisors reported that “they enjoy and maintain a reciprocal relation based on trust and that managing the relation is quite easy,” to such an extent that these partners in the exchange are conscious that “institutional trust (customer/bank) has not yet been really tested” due to the insignificance of the incidents encountered. Thus, customers expect that “the bank will answer positively our future needs (e.g. a credit request) and that the advisors will pay attention and remain aware of the evolution of our needs and expectations.”

Finally, this linear and cumulative way of building trust in the service relationship shows that the interpersonal trust stock between the client and the advisor makes it possible to absorb small-scale incidents that have been well managed by the bank and to perpetuate the relationship between the two partners.

Fig. 1 – Linear cumulative way of constructing interpersonal trust.

The second way to build interpersonal trust, referred to as the “by stages” process, relates to those situations where the incidents were mainly caused by customers, and were considered to be quite serious and/or were not satisfactorily resolved by the bank. These situations are characterized both by the client’s entry into relation with the current bank based on a strong predisposition to trust stemming from a perceived positive image of the bank and by a strong feeling of disappointment when testing the relationship through service encounters, resulting in an unsatisfactory resolution of major incidents by the bank advisor. As a result, clients’ confidence is reduced, with clients stating that they are loosing trust and “becoming suspicious” of the advisor’s reliability and the bank’s credibility.

73However, when the head of the bank branch intervenes to solve an incident caused by the advisor, the customer calls into question interpersonal confidence but not institutional trust. These customers end up having doubts and reconsidering their confidence progressively in the course of their experience with the new advisors whom they will subsequently meet. Interpersonal trust is then put to the test in relation to the behavior of the advisors during these various experiences. In such cases, advisors maintain that “management of the relation with these [vulnerable] customers is a daily battle” and that they need to be “very attentive to this type of customer, who is much more demanding than those who have not encountered a serious incident, in particular for ‘major customers’ in terms of profitability to the bank.”

At the conclusion of these incidents poorly managed by the advisor, the customer will no longer automatically place his/her trust in the latter, but will put it to the test at each service encounter because she/he believes that trust is earned and that the initial stock of interpersonal trust has been altered by the unsatisfactory management of the previous incidents encountered. However, institutional trust remains the safety net that can save and maintain the relationship with the client, which must be fed and reinforced by a new and peaceful interpersonal relationship with the advisor.

Fig. 2 – Transition from a “linear” to a “by stages”

means of building interpersonal trust.

3.4.3. Transfers of trust between institutional and interpersonal dimensions during the banking relationship

Finally, the discourse analysis shows some mechanisms for the transfer of trust from the institutional dimension to the interpersonal one during the banking relationship, based on the duration and the quality of customers’ previous banking relationship. Hence, the processes of trust building and development are strongly shaped by the temporal dimension of the banking relationship and the customers’ life trajectory.

Tendentially, the bank’s recent (generally young) clients attach more importance to institutional trust because the moment at which they entered into a relationship with the bank is still recent and they have not yet put to the test the solidity of their relationship. Thus, they do not consider interactions with the advisor to be important at this stage, either because they are just starting their relationship with the bank or because they consider that they have little experience with banks on which to base a clear perspective of the bank and its staff (they tend to be “students” or “young workers that have recently began their job life”).

Nevertheless, this young clientele still attaches great importance to the interpersonal trust with their advisor during the banking incidents they encounter (stage 3). Some of these customers provide an explanation linked to the lived context of vulnerability caused by a “life incident” resulting from short-term unemployment or a precarious occupation. This unstable (and negative) situation, from the bank’s perspective, tends to generate an automatic refusal of a loan request, which may finally be well managed by an empathetic and friendly bank advisor (e.g. authorization of an exceptional overdraft, loan repurchase, etc.). Other clients who have left their former bank following an incident caused by the bank are critical of the previous financial institution, stressing that the “real” relationship of trust is interpersonal and essentially exists between a client and her/his advisor. This trust is manifested in the discourse of clients who feel the need to trust their advisors as soon as they “place their savings in a bank” because of the asymmetrical relationship with the bank to their detriment.

Hence, during their relationship with the present bank, these customers become aware of the importance of interpersonal trust to such an extent that some of them follow their advisor when he/she moves to 75another branch. This institutional to interpersonal transfer of trust was observed for customers who had encountered banking incidents that were satisfactorily resolved by their advisor either at the time of entering, or in the course of the relationship, with the current bank. Thus, even if they say they maintain institutional confidence in the bank itself, their reliance on the advisor overcomes their trust in the bank as an institution.

On the other hand, clients who are generally more experienced and older, and who have encountered relatively few incidents (properly dealt with by advisors), have developed a kind of resilience in the face of life’s vicissitudes and in their banking relationship, prioritizing the institutional dimension of trust over the interpersonal dimension in their relationship with the bank. This is based on the fact that the incidents, seen as “not so serious” by these customers, are often caused by the bank and are generally correctly and quickly resolved by the advisors (e.g. “a checkbook not sent,” “agios reimbursed” because of an overdraft). These experienced customers tend to relativize past experiences with incidents more or less well managed by the advisors and by the claims department of the bank. These clients think that “they have learned to know how the bank works” such as the high turnover of the staff and the intervention of the branch manager in the event of a major problem occurs. They talk about “learning continuously about the relationship with the bank” and their confidence has not been significantly shaken by the incidents they have encountered.

These customers also explain their entry into the relationship with the present bank in terms of the perceived credibility of the institution. However, following their long experience of the banking relationship with various advisors, these customers tend to put past incidents into perspective to assess the quality of their service encounters with the advisor. They say “they have learned about the internal functioning of the bank and incidents’ management processes.” Thus, when a problem occurs that they might previously have considered to be serious, they highlight their “learning about the relation with advisors and the bank, which make them calmer because they know that their advisor will solve it successfully.” Even if this does not happen, they think that “the head of bank branch will be available if a problem arises with the advisor.” Their experience with the bank allows them to develop a certain resilience in the face of incidents encountered and to be confident in their resolution by the bank.

76In these cases, clients had not encountered incidents deemed “very serious,” or if they had, these incidents were on the whole dealt with satisfactorily by their advisors, and if not by the hierarchy, which takes into account their long-standing relationship with the bank and their status as a reliable client. Over time and through experiences that are considered globally positive, these old customers reveal their trust primarily in their bank rather than in their advisor. They “trust the bank that recruits good advisors first;” these clients do not consider it appropriate to follow these advisors if they move to another bank or branch. The institutional trust seems to structure their banking relationship because it is more perennial; although they remain sensitive to the quality of their interpersonal relationship with the advisor, they know that in the future he/she will have to change branch or even bank.

The status and polarity of interpersonal and institutional trust during the banking relationship are strongly linked to the situation of vulnerability in which the customer may find himself/herself, to the history of the relationship, and to the seriousness of incidents that this situation generates. Moreover, the way these problems were managed in this asymmetrical relationship, and the perceived justice associated to the resolution of the incident, testifies to the real willingness of the bank to establish a relationship based on trust with their clients and not to capture the value of the relationship to the clients’ detriment.

4. DISCUSSION AND RESEARCH IMPLICATIONS

This research improves the understanding of the status of trust and its evolution in the service relations between bank clients and their advisors during the vulnerable experiences of clients characterized by incidents generating a temporary fragility in their financial resources.

It is possible to position the findings of this research within the more general framework of services management. Thus, the factors that intervene in building interpersonal and institutional trust, identified in the banking relationship (duration of the relation, history and quality of past relationships, incidents’ seriousness and frequency, incidents’ management efficacy), can be applied more widely to the services sector. Any exchange relationship between a client and a service provider implies interactions between that client and the front office personnel (interpersonal trust) but also a relationship between that client and the 77provider, seen as a service brand (institutional trust), with the two feeding each other. The factors identified in this research represent the many levers that a service company can use to develop, preserve, or restore trust with its customers during their relationship and as a driver for a relevant segmentation of its vulnerable clientele.

On the theoretical level, to analyze trust in the customer–bank relationship, we adopted a time perspective, in contrast to earlier studies that have mainly used a static approach. This dynamic approach shows, following Huang and Wilkinson (2013), that trust changes depending on the experience and outcomes of the actions and interactions of the actors embedded within the relationship and also on other events taking place over time, both in the focal and connected relationships. Applying this approach to our empirical field enables us to examine the evolution of the status of trust during the course of the banking relationship and allows us to improve our understanding of the mechanisms of trust building and development by identifying two means of doing so. The first mode shows that a relationship based on trust can be built through a cumulative “linear” process when this relationship is not marred by incidents or when incidents are less serious and correctly and rapidly managed if they do occur. The second mode of trust construction, “by stages”, is characterized by relationships that suffer from significant incidents that were not satisfactory resolved by the bank. In this case, confidence is put to the test and may be progressively renegotiated by the partners in the course of their ongoing relationship. The inclusion of the time dimension in our analysis also makes it possible to reconcile contradictory results arising in the literature in relation to some concepts’ status, such as satisfaction, as an antecedent or consequence of trust, according to the stage of the relationship at which the investigation is undertaken. Finally, the study highlights how institutional trust is transferred into interpersonal trust in the banking relationship, depending on customers’ age and banking history, as well as the importance of the incidents encountered and how they were resolved.

This research also resonates with the recent work of Johns and Davey (2019) on value creation with vulnerable consumers in the services domain. These authors showed that front-line staff in services can act as an intermediary between the vulnerable client and the organization in service delivery when the client does not have, or is unable to mobilize, 78his/her resources (their own and those of the environment) to participate in the production of the service. Front-line staff can also play the role of a transformative apomediary when the personnel in contact with the clientele do not seek to substitute the customer in the production of the service, but aim instead to activate the client’s resources and capacities, even residual ones, in order to encourage her/him to participate. In the case of banks, these two roles have been identified in the interactions between vulnerable clients and bank advisors. Because of the imbalance of power in the banking relationship in the event of incidents occurring, we have reported situations where the advisor ruled against the client despite his/her previous situation being quite healthy without involving the client in the decision because the client was the source of the banking incident (more or less serious) due to his/her lived vulnerable situation. In other cases, the advisor was more benevolent and more conciliatory to the vulnerable client when the incident was deemed to be less serious, by developing satisfactory solutions in conjunction with client that were neither unfavorable to the client nor to the bank.

Our research raises some questions about the bank’s salesforce management. Particular attention must be paid to the turnover of advisors in the banking relationship in the French context, which should be of interest to practitioners and researchers in the field of services management. This raises questions regarding the ability of the various levers of interpersonal trust to improve and strengthen the link with customers when advisors change branches every three years, or even more often. Moreover, it underlines the boundaries of the relationship between the customer and the banking brand and of its potential nurturing through the personal relation developed with the front-line staff. While the banks are trying to develop the notion of brand in banking services through their communication policy, too much proximity between customers and advisors over the long term can encourage a detachment from the brand in favor of an attachment to the advisor, with potential defections by clients tempted to follow their bank advisors, thus weakening their relationship with the bank as an institution. This perspective is quite pertinent in the French context where the current strategy of banks encourages a high turnover of staff (in contact with the clients), which does not enable the role of advisors in the construction and reinforcement of the trust relationship to be fully taken advantage of and presents the 79risk of cannibalizing institutional trust by interpersonal confidence if such human connection occurs. Banks can thus find themselves faced with abuses linked to an over-involvement of advisors in their relations with certain clients with whom an affinity, or even a friendship, may emerge and which may not work in favor of the bank’s interests (e.g. granting a loan to a client even though he/she does not meet all the financial conditions imposed by the bank). The issue of control, both organizational over advisors’ practices (to avoid deviant behaviors) and interpersonal over the advisor’s behaviors and claims by clients, is therefore central to dealing with trust. In short, there can be no trust without (some mechanisms of) control.

In view of our results, the segment of vulnerable customers should not be considered by the market as an homogenous group to be treated uniformly, e.g. removing them from, or marginalizing them in, the market as soon as these customers encounter service incidents. In the banking sector, this segment represents, at least in part, a potential pool of profitable customers if it can benefit from appropriate support from the bank advisors in order to improve and re-normalize their position at the financial and social levels. Thus, offering vulnerable clients, whose medium- and long-term profitability is secured, a service adapted to their specific needs and to their transitory limited resources to help them cope with this situation, can help to restore or strengthen trust and build loyalty. Moreover, this strategy allows the bank to enhance its image of social responsibility, which is congruent with the mutualist positioning of the BRED bank studied. The way in which these clients are supported in terms of reception, listening, advice, education, and adapted service offerings represent important issues in the fight against social exclusion and the perceived sense of injustice when the bank and the advisor disregard the previous profitable relationship with these same clients before their banking incident had occurred. A client who rebounds becomes a full-fledged economic player once again, spreading positive opinions of the bank and generating gains.

Our findings suggest that banks should adapt their strategies to the various situations of vulnerability that their clients (including formerly profitable ones) may be going through and should better equip and assist advisors in the management of these more or less difficult portfolios over time. In the current context of a health and economic crisis that 80is generating a strong impoverishment among households, including those that were still stable a few months ago, bank advisors are increasingly called upon to manage tense relations with these precarious and vulnerable clients who are encountering difficulties in repaying their loans or meeting their incompressible expenses. They have to work with and help these clients, who were previously solvent, and who are now in more or less temporary financial difficulty, by proposing adapted financial products and services, providing advice and material assistance in managing current accounts, or helping them to rationalize their bank assets. To this end, banks must rethink the boundaries and roles of advisors’ responsibility/job with a view to providing them support (psychologically and materially) and training them to manage conflicts and situations of uncertainty generated by the increased precariousness of clients, while avoiding stigmatization, self-pity, or condescension towards them. Indeed, the increase in conflict situations with vulnerable clients generates tension and stress at work for bank advisors both psychologically (permeability to the problems of clients they have known and worked with for a long time) and physically (verbal incivilities, or even physical altercations).

Regarding their clientele, banks’ strategies and initiatives must encompass providing support for (potentially) vulnerable clients (including preventing them from entering into a state of vulnerability) and aiming to curb over-indebtedness and social exclusion. Some French mutual banks (e.g. Banques Populaires) have already embarked on experiments to open branches dedicated to highly vulnerable customers, both to provide long-term support for these “fragile customers” and decrease the risk of then getting bogged down or relapsing and to progressively help restore normal banking relations. In this case, they have been led to develop a “bottom of the pyramid” (BoP) strategy (Prahalad and Hart, 2002) based on banking products and service offerings adapted to the fragile situations of customers in order to help them adjust their behavior, re-socialize themselves, and limit both the risks of incidents and the costs associated with repeated overdrafts.

We advocate for public policy and banking practices’ changes to reduce the risk of the exclusion of vulnerable customers from access to the banking system, which is crucial to avoid these people becoming marginalized in the market. Vulnerable clients with potential should 81be kept within the bank’s client portfolio because of their short- or medium-term profitability, while public financial institutions and/or associative spheres, which are increasingly called upon to play an active role in alleviating the poverty and precariousness of individuals (Oosterlynck et al., 2013), should look after chronic vulnerable clients and help them to gradually reintegrate with the market, in particular by training them to rigorously manage their budget and, if necessary, to discipline their consumption behavior. These measures are the prerequisites for their reintegration into the market and into the banking system. Our advocacy towards public authorities and banks in favor of the inclusion of vulnerable clients echoes Sen’s (1985) work on the capabilities of customers in precarious (poverty) situations. For some of them (potentially profitable ones), localized support over time is enough to revive them, while for others (less profitable), it is necessary to deploy stronger, long-term measures. The task is certainly complicated because the causes of vulnerability are multifactorial, but this policy is necessary and salutary because the social, economic, and psychological stakes and costs for society are so high. The concerns, difficulties, and challenges related to this large segment of vulnerable customers provide practical guide for policy makers to solve social and economic problems related to the impoverishment of large segments of people. Besides public policy efforts, banking institutions should adjust their rules to embrace (at least temporarily) the vulnerable as a profitable market segment. Given their past economic situation and social position, they deserve to be better treated and helped to go through episodes of vulnerability. These efforts must involve all the stakeholders, including the clients themselves, in the analysis of their situation of vulnerability in order to explore with them their own efforts and arbitrations to deal with this critical situation and to find together a sustainable and inclusive resolution to the problems encountered in the course of the service relationship. While this research focuses on financial vulnerability, future research can examine health (disabilities), ageing, joblessness, or illiteracy vulnerabilities, which can be cumulative with financial vulnerability, in terms of their contribution to excluding people from the market.

825. LIMITATIONS AND RESEARCH AVENUE

This research has the advantage of being based on a longitudinal and retrospective approach that shows the evolution of the relationship between vulnerable clients and bank advisors and the arrangements put in place to manage episodes of vulnerability experienced by clients. Certain situations, however, notably when trust between the exchange partners is broken and customers may leave the relationship following unresolved or poorly managed banking incidents, were not well documented. This stems from a limitation of our research in that it failed to include in the sample of clients surveyed those who had experienced serious incidents that were not or were poorly managed by the bank, thereby altering the interpersonal and institutional trust that existed and leading to a breakdown in their relationship with the bank. It is likely that clients who were highly dissatisfied with their relationship with the bank and the advisors declined the invitation to participate in the study and that, ultimately, only those clients who had experienced less serious incidents and/or quite serious incidents but received satisfactory attention and resolution were willing to be included in the study. Consequently, it is clear that cases of dissolution of the relationship and alteration of trust between vulnerable clients who were dissatisfied with the treatment (unworthy, disrespectful) reserved for them and who left the banking relationship, are minorized, or even hidden, in our results. This opens up a research perspective centered around these customers’ profiles, which is certainly difficult to access, but which can potentially be approached via the public structures that support over-indebted people. A final avenue of research would be to question the place of emotions in the vulnerable customer–bank advisor relationship in so far as their exchanges and interactions during episodes of vulnerability give rise to intense emotions on both sides that can encompass either compassion and empathy or conflict and anger, which may disrupt the relationship and lead to a reconsideration of trust between the parties.

83REFERENCES

Amine A., Gatfaoui S. (2019), “Temporarily vulnerable consumers in a bank services setting”, Journal of Services Marketing, vol. 33, no 5, p. 602-614.

Andaleeb S. (1991), “Trust and dependence in channel relationships: Implications for satisfaction and perceived stability”, AMA Summer Educators Conference Proceedings, p. 249-250.

Anderson L., Ostrom A. L. (2015), “Transformative service research: advancing our knowledge about service and well-being”, Journal of Service Research, vol. 1, no 3, p. 243-249.

Anderson L., Ostrom A. L., Corus C., Fisk R. P., Gallan A. S., Giraldo, M., Mende, M., Mulder, M., Rayburn, S. W., Rosenbaum, M. S., Shirahada, K., Jerome, W. D. (2013), “Transformative service research: an agenda for the future”, Journal of Business Research, vol. 66, no 8, p. 1203-1210.

Baker S. M., Gentry J. L., Rittenberg T. L. (2005), “Building understanding of the domain of consumer vulnerability”, Journal of Macromarketing, vol. 25, p. 128-139.

Bergadaa M., Graber S., Muhlbacher H. (1999), “La confiance dans la relation tripartite vendeur-client-entreprise”, Working Paper 99.5, École des Hautes Études Commerciales, Universite de Geneve.

Berry L. L. (1995), “Relationship marketing of services—growing interest, emerging perspectives”, Journal of the Academy of Marketing Science, vol. 23, September, p. 236-245.

Besson M., Gurviez P. (2000), “La vente dans un contexte relationnel: l’exemple du luxe”, Décisions Marketing, vol. 20, Mai-Août, p. 47-55.

Bitner M. J., Booms, B. M., Tetreault M. S. (1990), “The service encounter: Diagnosing favorable and unfavorable incidents”, Journal of Marketing, vol. 54, January, p. 71-84.

Brenkert G. (1998), “Marketing and the vulnerable”, Business Ethics Quarterly, vol. 1, p. 7-20.

Chaudhuri A., Holbrook M. B. (2001), “The chain of effects from brand trust and brand affect to brand performance: The role of brand loyalty”, Journal of Marketing, vol. 65, no 2, p. 81-93.

Couret, D., Metzger, P. (2009), “Réduire les vulnérabilités plutôt qu’éradiquer la pauvreté. Le modèle de développement néolibéral à l’épreuve de la ville des pays du Sud”, Espace, Populations, Sociétés, vol. 2, p. 263-277.

84Deloitte -Étude- (2019), Relations banques et clients, 9e edition, 18 Septembre 2019, available at: https://www2.deloitte.com/fr/fr/pages/presse/2019/entre-open-banking-et-humain-la-banque-a-un-nouveau-role-a-jouer.html (accessed 26 december 2020)

Deutsch M. (1958), “Trust and suspicion”, Journal of Conflict Resolution, vol. 2, no 4, p. 265-279.

Doney P. M., Canon J. P. (1997), “An examination of the nature of trust in buyer-seller relationships”, Journal of Marketing, vol. 61, no 4, p. 35-51.

Dwyer F. R., Schurr P. H., Oh S. (1987), “Developing buyer-seller relationships”, Journal of Marketing, vol. 51, no 4, p. 11-27.

Eiglier P., Langeard E. (1987), Servuction: Le marketing des services, Paris, Ediscience.

Flanagan J. C. (1954), “The critical incident technique”, Psychological Bulletin, vol. 51, no 4, p. 327-358.

Ganesan S. (1994), “Determinants of long-term orientation in buyer-seller relationship”, Journal of Marketing, vol. 58, no 2, p. 1-19.

Geyskens I., Steenkamp J.-B. (1995), “An investigation into the joint effects of trust and interdependence on relationship commitment”, Proceedings of the 24th Annual Conference of the European Marketing Academy, p. 351-371.

Gondard-Delcroix C., Rousseau S. (2004), “Vulnérabilité et stratégies durables de gestion des risques: une étude appliquée aux ménages ruraux de Madagascar”, Revue Développement Durable et Territoires, vol. 3, available at: http://developpementdurable.revues.org/1143 (accessed 23 September 2017).

Granovetter M. (1985), “Economic action and social structure: The problem of embeddedness”, American Journal of Sociology, vol. 91, no 3, p. 481-510.

Grönroos C. (1990), Service Management and Marketing. Managing the Moments Of Truth in Service Competition, Lexington, Lexington Books.

Guibert N. (1999), “La confiance en marketing: Fondements et applications”, Recherche et Applications en Marketing, vol. 14, no 1, p. 1-19.

Hess J. (1995), “Construction and assessment of a scale to measure consumer trust”, in Stern, B. B., Zinkhan, G. M. (eds.), AMA Educators’ Proceedings: Enhancing Knowledge Development in Marketing, vol. 6, Chicago, American Marketing Association, p. 20-25.

Huang Y., Wilkinson I. F. (2013), “The dynamics and evolution of trust in business relationships”, Industrial Marketing Management, vol. 42, no 3, p. 455-465.

Ipsos / Secours Populaire (2020), Baromètre de la pauvreté Ipsos / Secours Populaire 2020: quel impact de la crise sanitaire sur la précarité en France?, September, available at: https://www.ipsos.com/fr-fr/barometre-de-la-pauvrete-ipsos-secours-populaire-2020-quel-impact-de-la-crise-sanitaire-sur-la (accessed 24 november 2020)

85Johns R., Davey J. (2019), “Introducing the transformative service mediator: Value creation with vulnerable consumers”, Journal of Services Marketing, vol. 33, no 1, p. 5-15.

Keaveney S. M. (1995), “Customer switching behavior in service industries: An exploratory study”, Journal of Marketing, vol. 59, April, p. 71-82.

Lovelock C., Lapert D. (1999), Marketing des services. Stratégie, outils, management, Paris, Publi-Union.

Mayaux F., Flipo J.-P. (1995), “Marketing des services: rien à faire sans la confiance”, in Gomez P.-Y., Bidault F., Marion G. (eds.), Confiance, entreprise et société: mélanges en l’honneur de Roger Delay Termoz, Paris, Éditions Eska, p. 151-163.

Mayer R., Davis J., Schoorman F. (2007), “An integrative model of organizational trust”, The Academy of Management Review, vol. 20, no 3, p. 709-734.

Moorman C., Zaltman G., Deshpandé R. (1992), “Relationship between providers and users of market research: The dynamics of trust within and between organizations”, Journal of Marketing Research, vol. 29, no 3, p. 314-328.

Morgan R. M., Hunt S. D. (1994), “The commitment-trust theory of relationship marketing”, Journal of Marketing, vol. 58, p. 20-38.

Oosterlynck S., Kazepov Y., Novy A., Cools P., Barberis E., Wukovitsch F., Sarius T., Leubolt B. (2013), “The butterfly and the elephant: local social innovation, the welfare state and new poverty dynamics”, ImPRovE Working Paper [13/3], Antwerp University, Antwerp, April.

Pavia T. M., Mason M. J. (2014), “Vulnerability and physical, cognitive, and behavioral impairment: Model extensions and open questions”, Journal of Macromarketing, vol. 34, no 4, p. 471-485.

Prahalad C. K., Hart S. L. (2002), “The fortune at the bottom of the pyramid”, Strategy+Business, January 10, First Quarter, no 26, p. 2-14.

Ring P. S., Van de Ven A. H. (1992), “Structuring cooperative relationships between organizations”, Strategic Management Journal, vol. 13, no 7, p. 483-498.

Ring P. S., Van de Ven A. H. (1994), “Development processes of cooperative interorganizational relationships”, Academy of Management Review, vol. 19, no 1, p. 90-118.

Ringold D. J. (1995), “Social criticisms of target marketing: Process or product”, American Behavioral Scientist, vol. 38, February, p. 578-592.

Rosenbaum M. S., Seger-Guttmann T., Gilardo M. (2017), “Commentary: Vulnerable consumers in service settings”, Journal of Services Marketing, vol. 31, no 4/5, p. 309-312.

86Rosenbaum M. S., Corus C., Ostrom A. L., Anderson L., Fisk R. P., Gallan A. S., Giraldo M., Mende M., Mulder M., Rayburn S. W., Shirahada K., Williams J. D. (2011), “Conceptualization and aspirations of transformative service research”, Journal of Research for Consumers, vol. 19, p. 1-6.

Rousseau D. M., Sitkin S. B., Burt R. S., Camerer C. (1998), “Not so different after all: A cross-discipline view of trust”, The Academy of Management Review, vol. 23, no 3, p. 393-404.

Sen A. K. (1985), Commodities and Capabilities, New York, Oxford University Press.

Schilke O., Cook K. S. (2013), “A cross-level process theory of trust development in interorganizational relationships”, Strategic Organization, vol. 11, no 3, p. 281–303.

Smith N. C., Cooper-Martin E. (1997), “Ethics and target marketing: The role of product harm and consumer vulnerability”, Ethics and Target Marketing, vol. 61, July, p. 1-20.

Wang J. J., Tian Q. (2014), Consumer vulnerability and marketplace exclusion: A case of rural migrants and financial services in China”, Journal of Macromarketing, vol. 34, no 1, p. 45-56.

Williamson O. E. (1993), “Calculativeness, trust and economic organization”, Journal of Laws and Economics, vol. 36, April, p. 453-486.

Zajac E. J., Olsen C. P. (1993), “From transaction cost to transactional value analysis: Implications for study of interorganizational strategies”, Journal of Management Studies, vol. 30, no 1, p. 131-145.

1 Corresponding author.

2 Ipsos poll based on a representative sample of 1,002 French people aged 16 and over interviewed on September 4 and 5, 2020 : quota method based on gender, age, occupation of the household reference person, region, and category of agglomeration (Ipsos / Secours Populaire, 2020).

3 BRED Banques Populaires is a French mutual bank.

- Thème CLIL : 3306 -- SCIENCES ÉCONOMIQUES -- Économie de la mondialisation et du développement

- ISBN : 978-2-406-12052-0

- EAN : 9782406120520

- ISSN : 2555-0284

- DOI : 10.48611/isbn.978-2-406-12052-0.p.0055

- Éditeur : Classiques Garnier

- Mise en ligne : 23/06/2021

- Périodicité : Semestrielle

- Langue : Anglais

- Mots-clés : Clients vulnérables, banques, confiance, relations de services, stratégies relationnelles, inclusion sociale, France