Relation de service, boucle de service et bouquet de services examinés dans un contexte logistique

- Type de publication : Article de revue

- Revue : European Review of Service Economics and Management Revue européenne d’économie et management des services

2021 – 2, n° 12. varia - Auteurs : Mevel (Olivier), Morvan (Thierry), Morvan (Nélida)

- Pages : 35 à 68

- Revue : Revue Européenne d’Économie et Management des Services

Service relationship, service loop

and service package examined

in a logistics context

Olivier Mevela

Thierry Morvanb

Nélida Morvanb

aLEGO, Bretagne Occidentale University, France

bRennes I University, France

Introduction

In various industries, such as aeronautics, automotive, and textiles, Logistics service providers (LSPs) have become key players with the necessary capabilities to boost and optimize today’s supply chains that are now multi-actor and, as a consequence, complex and more geographically extensive (Camman etal., 2017; Fulconis and Saglietto, 2015). These specialized actors control flows by taking on an intermediation role between one or several customer(s) and between suppliers specialized in transport and warehousing activities. They also develop logistics solutions adapted to the sometimes very specific requests from customers (Dai etal., 2020; Fabbe-Costes and Roussat, 2011; Saglietto and Cézanne, 2015). Contemporary LSPs are “architects”, “orchestrators”, or 4PLs (fourth party logistics providers) (Fattam and Paché, 2017).

Food supply chains are also part of this changing landscape in the logistics services sector. Manufacturers and large retailers are no longer content with “basic” logistics services (transport and storage) and are 36now looking to LSPs to manage more complex logistics processes. More specifically, faced with current retailer requirements (fixed circuits, deliveries to a wide variety of store formats, etc.) and a fiercely competitive environment (acceleration of product innovation, pressure on prices, etc.), agri-food industries are looking for LSPs with the capability to build efficient organizational models that control logistics costs. These organizational models must also be sufficiently tailored to their specific needs (volumes to be transported, seasonality, deliveries in consumption zones, etc.). Such manufacturer requirements underline the complexity of the service relationship to be co-constructed and implemented. Indeed, LSPs must find a balance between efficiency and customization of a predominantly material service, despite the development of dematerialized LSPs that assign activities with a lower added value to low-costplayers (Camman etal., 2017). Finding this balance is closely linked to the level of service that is expected and perceived by the manufacturer (Shi etal., 2018; Sohn etal., 2017). Therefore, the LSP’s capability of innovation, in terms of service offering, is likely to improve the quality of the logistics services perceived by the manufacturer (Ali and Kaur, 2018; Sohn etal., 2017).

Consequently, in terms of service relationships, the series of customer expectations and the LSP’s capabilities to meet them appears to be the key element in proposing a relevant service that meets the customer’s exact needs (Baranger etal., 2016). This raises the question of the LSP creating the right service package to establish a long-lasting service relationship with the customer (Grönross, 2000). Any service is actually rendered on the basis of a “service package”, i.e. the sum of the parts that will “deliver service” (Lovelock etal., 2014). Therefore, the customer will be responsive to a value proposition, which is itself backed by service packages. The latter must incorporate a certain number of attributes that are central to the logistics services; attributes that are ultimately sources of varying degrees of added value perceived by the manufacturer.

However, in the food industry there is a tight competitive environment coupled with a highly restrictive logistics environment in the fresh and ultra-fresh sectors. Against such a background, manufacturers require a constantly guaranteed logistics service rate from the LSP, appropriate solutions according to the type of flow processed, and all at a reasonable 37price. Therefore, the LSP has to develop a relevant service package that meets manufacturers’ logistics requirements (transport costs, traceability, supply chain performance, etc.). Therefore, through the concepts of service relationship, service loop and service package, the present article will identify the components of the service packages of LSPs operating in food supply chains, and then define how the production of LSP logistics services is likely to evolve.

To answer this research question, an empirical survey was conducted among manufacturers in the agri-food industry. The first objective was to analyse manufacturers’ perceptions of service quality and of customization of the relationship, with the aim of evaluating the different service packages proposed. The second objective was to bring to light expectations not covered by the LSP. The first part of the article sets out to gain a more in-depth understanding of the specificities of the service production system of LSPs operating in the food industry. The second part presents the empirical aspects related to the survey methodology and the results of a quantitative empirical study. The third part will discuss theoretical and managerial implications.

1. LSPs in the agri-food industry: key players

1.1. The specificities of LSPs in food supply chains

Since the 1990s, in the food industry, the continued retailer interest in logistics has led to significant changes in multi-actor supply chains that have been disrupted by fundamental changes to the traditional organization of distribution once controlled by manufacturers (Chanut and Paché, 2012; Filser etal., 2020). As retailers are becoming increasingly powerful in the channel, manufacturers are finding themselves in the position of having to deliver to retailer platforms. It is important to note that the deliveries made must take into account shorter transport times, the generalized reduction in batch size transported, and the need to preserve use-by dates (Bonacich and Wilson, 2005). Therefore, in order to differentiate themselves from their competitors, manufacturers need to rely on LSPs that can offer a logistics service that is flexible, 38responsive and creative (Kacioui-Maurin etal., 2016; Wagner and Sutter, 2012; Wallenburg and Lukassen, 2011).

Moreover, by disengaging from transport and logistics activities, which are now considered secondary in fresh produce value chains, manufacturers and large retailers have encouraged the emergence of new actors specialized in logistics: LSPs. LSPs have become indispensable organizations in the functioning of food supply chains (Filser etal., 2020; Hiesse, 2015; Mehman and Teuteberg, 2016). More specifically, by positioning themselves at the intersection of several supply chains, LSPs are therefore likely to offer logistics solutions based on their capability to consolidate the volumes of the various shippers that use their services, with a view to benefiting from economies of scale. Moreover, through their capability to innovate, manufacturers and large retailers want them to be a proactive force on services offered, and on technologies and logistics processes deployed (Cichosz etal., 2017; Dai etal., 2020; Kacioui-Maurin etal., 2016; Wagner and Sutter, 2012; Wallenburg and Lukassen, 2011).

These profound changes in the role of the LSP in supply chains with specific and demanding characteristics (no break in the cold chain, product shelf life, short response time between order and delivery, etc.) emphasizes the fact that it is developing a specific service offering. The service offering includes traditional temperature-controlled transport activities: courier service and transport of batches (full or half batches). In addition to these traditional activities in the provision of temperature-controlled transport services, LSPs are rapidly expanding their offer to include commercial activities (co-packing, contract packaging), information management activities (tracking and tracing), industrial activities (co-manufacturing), and organizational engineering activities (infrastructure audit, information systems consulting, etc.). LSPs can also propose customer-specific logistics solutions (Dai etal. 2020; Duong and Paché, 2015; Hiesse, 2015). Also, based on the categorization proposed by Accenture, the diversity of somewhat complex roles can be summarized according to the type of service offered by the LSP in the field of temperature-controlled transport (seeTable 1).

39Tab. 1 – LSP categories, type of service offered, actors and specificities

of the logistics services in the field of temperature-controlled transport.

|

LSP Category |

Type of service offered |

Role of LSP |

LSP in the field of temperature-controlled transport |

Offering proposed in the field of temperature-controlled transport |

Strategy developed by the LSP in the field of temperature-controlled transport |

|

1PL (first party logistics) |

Basic services: transport or storage. |

Simple implementation of transportation- or storage-related operations. |

Local LSPs |

Collection and (local or national) distribution activities by supplying the networks of specialized groups that are market leaders. |

Proficiency in local collection routes, responsiveness and flexibility to respond to customers. |

|

2PL (second party logistics) |

Basic services: transport and storage. |

Simple implementation of transportation- and storage-related operations. |

|||

|

3PL (third party logistics) |

Basic services: transport or storage. Value-added services: activities of a commercial nature (e.g. after-sales service), industrial (e.g. delayed differentiation), administrative (e.g. customs) or informational (product and logistics traceability). |

Implementation of logistics operations. Integration of value-added services. |

Regional LSPs (Mesguen, Antoine, etc.) |

Geographic focus on certain logistics routes to the main consumption zones. Specialization in some segments in their activity zones (seafood products on the coast, etc.). |

Building a customized offering: proficiency in certain routes, focus on relational quality, etc. |

| 40

4PL (fourth party logistics) |

Global and made-to-measure logistics services of an informational nature. |

Design of logistics planning and information systems. |

Groups specialized in refrigeration (STEF, STG, etc.). Generalists (XPO, Kuehne+ |

Proposal of a global offering: ownership of dense networks, collections, massification, national or international deliveries, etc. Proposal of different types of warehouses: multi-format, multi-temperature, dedicated customer- warehouses. Implementation of traceability solutions. |

Standardizing the logistics solutions proposed via information systems. Developing the various refrigeration trades for specialists. Developing food e-commerce and urban logistics activities. Diversification strategy for generalists. |

From this table, it appears that shippers have a set of LSPs at their disposal who are likely to meet their expectations. These LSPs must be able to offer services the key elements of which are frequency of delivery, speed, flexibility, a built network, and regular lines offered, in order to meet the manufacturers’ requirements and their spatial practices. Through their strategic intelligence, they must also have the capability to offer ever more innovative and customized services to satisfy customer needs while investing in adequate logistical means (transport, information systems, warehouses, etc.) (Wagner and Sutter, 2012; Wallenburg and Lukassen, 2011).

1.2. LSP characteristics according to service theory

The very premise of providing logistics services involves the co-production of a service, i.e. a close temporal overlap between the consumption and production of the delivered service (Baranger etal., 2016). More specifically, a review of the theory of service literature shows the very essence of the service activity to be a global, time-bound process that does not have an autonomous existence outside of the provider-customer relationship (Baranger etal., 2016). Such a process is sequenced in three phases: request from the customer, mobilization of resources, and implementation of the service (Lovelock etal., 2014; Volle, 2000).

Thus, the service relationship initiated by the LSP takes concrete form through a characteristic, one-to-one process, during these three sequential phases, each phase being an opportunity to show the manufacturer the company’s competitive advantages, which could be the skills of the front-line staff who deliver the service, but also the material resources, such as the individual and collective skills to carry out the service, etc. (Mevel and Morvan, 2018). Therefore, in logistics service delivery what creates value is the delivery process seen as a whole. Since the logistics service delivery process is carried out by the service provider with their customer’s assistance, proper service performance depends on the collaboration between both protagonists from the point in time when the customer becomes a stakeholder in the service.

Moreover, this specificity of the service relationship induces very typical effects on the practices of LSPs, i.e. that service and production (“servuction”) is consumed synchronously. This specificity explains the importance given by service providers of information systems based on technologies that communicate (EDI, Web-EDI, labelling, etc.) in the context of operational 42management of service production in the logistics world (Elten etal., 2010; Olah etal., 2018). In addition, logistics services activities confirm the concept of the lack of storage facilities for this type of service. Nevertheless, material support and/or infrastructure can always be used to shift the time of the servuction to the end customer. This intangible dimension of the logistics service is further strengthened when the informational dimension of the service is operationally strong (Blanquart and Burmeister, 2009).

Through this service relationship, the question is also raised of identifying the support for the relationship initiated by the LSP. Indeed, service “support” can take a variety of forms: material, personal, informational or cognitive (Djellal and Gallouj, 2007). However, regardless of the service company studied, two major elements stand out: firstly, the level of interaction with the front-line staff, highlighting the somewhat intensive aspect of the service relationship initiated with the customer, and secondly, the material or conversely informational (and therefore immaterial) content of the logistics service (Baranger etal., 2016). It should be pointed out that the level of presence of front-line customer-facing staff will clearly define the degree of “made-to-measure” that the service is supposed to guarantee (Abramovici and Suquet, 2015; Lovelock etal., 2014). This leads to a classification of service types into four distinct categories, which gives a fairly complete picture of what may be the components of the different service packages developed by companies in the services sector. It also allows us to clearly position the activity of logistics services in the services world (see Table 2).

Tab. 2 – Typology of service companies and LSP positioning.

Source: adapted from Baranger et al. (2016).

|

Level of presence of front-line staff |

|||

|

Strong |

Low |

||

|

Nature of the service |

Material |

Cleaning, security, medical services, prestigious hotels or restaurants, etc. Logistics services providers (3PL) |

Hypermarkets, fast food, public transport, etc. Logistics services providers (1PL and 2PL) |

|

Immaterial (informational) |

Consulting, Audit, Legal Services, Education, etc. Logistics services providers (4PL) |

TV channels, Cinema, Internet service providers, GPS tracking |

|

Consequently, logistics services appear more clearly as a material service, whose production is industrialized to different degrees in the case of the 1, 2 and 3PLs if we use the typology proposed by Accenture; the 4PLs are committed to offering a more immaterial service in the form of consulting while subcontracting the more material aspects of the logistics services. In the case of logistics services, the key elements will therefore diverge according to the positioning of the LSP (seeFigure 1). More precisely, the key elements that prefigure the establishment of a service relationship in the world of logistics are the nature of the material service rendered (trucking, warehousing, storage, flow management, product traceability, logistical traceability, etc.) and the low level of presence of the front-line staff involved in the servuction process (joint service and production) for 1PLs and 2PLs. The level of presence of front-line staff increases for 3PLs because the skills mobilized require considerable expertise with respect to the value-added services developed. Finally, the 4LSPs offer genuine expertise by focusing on co-constructed made-to-measure services likely to initiate long-lasting relationships, and which are sources of value-added for the LSP and the manufacturer (Blanquart and Burmeister, 2009; Cichosz etal., 2017; Zacharia etal., 2011).

Next, all services are rendered from a set of elements that will prove to be more or less useful to the customer: services offered and intensity of the relationship. These two elements make up the service package (Baranger etal., 2016; Eiglier and Langeard, 1987; Gadrey, 1996; Lovelock etal., 2014; Volle, 2000), in which the customer evaluates and distinguishes between the key service1 and the secondary services offered to them. As a result, a variety of components produce the logistics service sought by the customer, components which are all centred around a core which covers the main use and utility requirements that the customer has for the logistics services. In line with the flower of service model (Lovelock et al., 2014), the various additional services offered to the customer can be seen as “petals” – add-ons or complements to the basic logistics service.

44The intensity of the relationship is also another constituent element of this service package. It materializes at the moment when the manufacturer interacts with the LSP, a moment during which the contact is likely to increase. The question then arises of whether or not to customize the response provided to the customer, according to the level of complexity of the service; a customization implemented by front-line staff who are more or less expert and qualified. For example, in the case of a customized service relationship, each manufacturer must be able to request different, adapted and customized processes (Mevel and Morvan, 2018). Also, depending on the resources (human, material or informational) mobilised in the front office (front-line actors, the material and/or immaterial supports, etc.), different services are likely to be proposed. For example, the production process of the logistics service may highlight the expertise of its front-line staff (proposals for informational services such as consulting) or, on the contrary, valorise the quality of the support proposed (means of transport, storage facilities, agency networks, etc.).

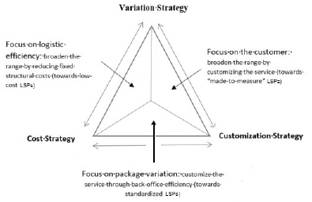

Finally, choosing a service package consists of the LSP adopting a specific positioning strategy bound by each corner of the strategic service triangle (see Figure 1), or a strategic positioning defined by a mix between cost orientation, level of customization, and choice of degree of variety and quality by segmenting the offering proposed. Three zones will then emerge (seeFigure 1) (Baranger etal., 2016). The “low-cost” service package favours efficiency through the mass of flows provided. The innovation- and customization-focused service package meets the needs of shippers who want to be supported in their development by LSPs. These LSPs must have the capability to offer ever more innovative and customized services while investing in adequate logistical means (transport, information systems, warehouses, etc.). As for the predominance of the quality/price ratio service package, this is a hybrid package, situated halfway between a low-cost and a service-based model, which is based on a rationalization of the offering and on a fair and reasonable pricing policy based on forecasts made upstream. The strategic service triangle shows, in terms of service manufacturing, the strategic alternatives that can be envisaged for an LSP aiming to characterize its service package around a few distinctive skills.

45

Fig. 1 – The strategic service triangle.

Source: adapted from Baranger et al. (2016).

Therefore, depending on the service package envisaged, the production of logistics services by LSPs requires the mobilization of specific resources and skills during the phases of request, mobilization and implementation of the service as summarized in the following table (seeTable 2) (Mevel and Morvan, 2011).

46Tab. 3 – Differentiating request, mobilization and implementation phases

for the three service packages proposed.

|

Service package features |

Customer request phase |

Staff mobilization phase |

Service implementation phase |

|

|

Logistics service package with focus on information systems |

Low-cost service package Focus on an automated and standardized information system. Objective of minimizing costs. |

Automated, EDI, web EDI, intranet. |

Very low intensity. Operational management through procedures. |

Optimizing capability of processing flows. |

|

Hybrid logistics service package with focus on quality/price ratio |

Hybrid package, standardized Rationalizing the offering. Fair and reasonable pricing policy (yield management). |

Standardizing response made to customer. |

Average intensity based on standardizing staff skills. |

Standardizing flows using information systems. |

|

Logistics service package with a focus of knowledge |

Customized service package Proficiency in informational complexity. Capability to innovate. |

Expertise of front-line staff. |

Very intense relationship with customer. Operational management through made-to-measure solutions. |

Quality and customization of service. |

Source: The authors.

472. Empirical investigation

2.1. Methodology

To study the characteristics of the service packages and their evolution, an empirical survey was conducted among manufacturers in the food industry in France, specifically in the Grand Ouest region (Brittany, Pays de la Loire, Normandy). The developed questionnaire had three main parts: the first part consisted in assessing the quality of the logistics service provided by the main LSP. The Montebello method (2003) was chosen to measure the perceived quality of service, called customer value added (CVA). To determine the CVA, it is necessary to list the attributes (sources of CVA) valued in each provider’s service package, determine their respective importance in the purchase decision, and ask customers to rate each attribute on a scale of 0 to 10. It is important to specify that sources of CVA had already been identified from a series of semi-structured interviews conducted with logistics managers during the first survey conducted in 2010 (Mevel and Morvan, 2010). At the end of these first interviews, a set of criteria (responsiveness to urgent deliveries, average delivery times, etc.) were identified and analysed and linked to nine main sources of CVA (seeAppendix 1). Then, during the second survey, it was checked whether there had been any significant changes in the list of CVA sources. The semi-structured interviews revealed that the characteristics of the sources of CVA remained unchanged (seeAppendix 1).

The objective of the second part of the study was to evaluate the criteria for customizing the LSP-manufacturer relationship. The criteria selected were2: LSP’s capability to adapt, level of satisfaction with the logistics service rate over the last five years, General Terms and Conditions of Sale, LSP responsiveness with regard to the different occasional territory-specific constraints, and finally, LSP responsiveness to disputes. These criteria were evaluated on a rating scale from 0 to 10. For the criterion “level of satisfaction with the logistics service rate over the last five years” a 10-point satisfaction scale was used (0 corresponding to “not at all satisfied” and 10 48to “completely satisfied”). The last part of the questionnaire was designed to determine the reasons why some manufacturers only worked with an LSP once, and the expectations not covered by the LSP.

From the data collected, a principal component analysis was conducted on all variables allowing the manufacturer to evaluate its main LSP. The variables selected are the weighted scores of the nine sources of CVA that shippers gave their main LSP and the five variables reflecting the LSP’s capability to customize the service. Then, to determine the possible existence of groups of manufacturers with some homogeneity, a non-hierarchical typology was carried out using the different variables revealed. This typology of the perception that manufacturers have of their main LSP makes it possible to identify the sticking points that LSPs will have to work on in order to better satisfy the manufacturers. The results presented below concern 112 manufacturers in the Grand Ouest region of France. As there is no reliable sampling frame on companies in the agri-food industry, a non-probabilistic method was adopted that is similar to a convenience sampling method (Jolibert and Jourdan, 2011). As such, existing business directories were used to contact manufacturers in these three regions and an average response rate of 20% was obtained for the sample. The profile of the group of companies that responded to the questionnaire is presented in Appendix 1.

2.2. Results

2.2.1. Service package in the field of temperature-controlled transport: manufacturer characteristics and expectations

The first result concerns more specifically the relative importance of the different components (CVA sources) of the service package proposed by an LSP in the field of temperature-controlled transport (seeTable 4). First, it was noted that three main criteria stand out as sources of CVA: capability to deliver the service, logistics service rate, and proposed rates. This result highlights that the LSP must differentiate itself in its operational deployment based on these three sources of CVA. More specifically, the importance given to the “capability to deliver the service” item underlines the fact that the manufacturer expects a guaranteed availability of means of transport and infrastructure despite variability, 49unpredictability, splitting of batch sizes, increase of “product” references, etc. Respecting logistics service rates is also one of the manufacturers’ priorities with regard to retailers’ requirements in terms of delivery frequency and timeframes for their platforms. The importance given to the criterion of “proposed rates” is due to the pressure on sales prices exerted by large retailers during commercial negotiations.

Tab. 4 – Importance of sources of CVA according to manufacturer

and average scores attributed to their LSP.

|

CVA source |

Importance of CVA sources |

Average scores for CVA sources |

|

Capability to deliver the service |

15.2% |

8.05 |

|

Logistics service rate |

14.9% |

7.95 |

|

Proposed rates |

13.5% |

6.89 |

|

Relational and commercial quality with the company |

11.5% |

7.69 |

|

Technical expertise |

11.1% |

7.35 |

|

Territorial control |

10.6% |

7.77 |

|

Information systems made available |

9.7% |

7.26 |

|

Reputation |

6.9% |

7.54 |

|

Eco-efficiency |

6.8% |

6.46 |

|

Overall average score |

7.17 |

Three other criteria stand out as discriminatory items in the service package offered by the LSP. These are primarily:

– Building long-lasting relationships (CVA source: relational and commercial quality of the relationship with the company). While technological innovations appear to be the most tangible and valorising manifestation of the LSP, the manufacturer is looking for a more customized relationship, one that is built on a daily basis3 and over a long period of time. Such a relationship allows the LSP to 50–respond to unforeseen situations while continuously improving the service package offered to the manufacturer.

– Guaranteeing product integrity and quality (CVA source: expertise). Manufacturers are looking for an LSP with the capability to constantly guarantee product freshness, a major source of differentiation in a fiercely competitive environment. As such, large retailers continuously evaluate a manufacturer on its capability to supply goods with the longest possible use by dates.

– Offering a dense network of logistics agencies (CVA source: territorial control). As regards its positioning, territorial control is also a discriminatory factor in the choice of manufacturer, who expects the LSP to provide services according to the specificities of the supplies to be delivered and the urgency, by relying on a physical network and adapting to all situations and for all destinations (regional, national and international).

Finally, the last three items of the service package to be offered by any LSP in the field of temperature-controlled transport have a more abstract positioning: information system, reputation and eco-efficiency. Thus, the information system is positioned in such a way that it cannot be considered as an autonomous and permanent source of differentiation. Indeed, it is directly incorporated into the main service offered to the customer. Technology-intensive information systems are essential for managing highly constrained interfaces and for monitoring product and logistics traceability. However, they do not seem to be a service that is likely to enhance the proposed offering. Although the “eco-efficiency” item highlights a manufacturer’s concern for the environment linked to their shipments, they are nevertheless focused on more immediate logistic problems in terms of deadlines, reliability, costs, etc.

The second result concerns the manufacturer’s evaluation of the intensity of the relationship co-constructed with the LSP (seeTable 5). Two criteria seem to be particularly poorly rated: the “General Terms and Conditions of Sale” and “responsiveness in the event of a dispute”. Indeed, only 22% of companies consider their LSP’s General Terms and Conditions of Sale to be good or very good, with the majority (72% of manufacturers questioned) considering them to be moderately good. 51For responsiveness in the event of a dispute, 37% emphasized that this was fairly satisfactory, while 53.7% gave it a more mixed assessment.

For the other criteria, only “capability to adapt” (average: 7.71) has a more favourable rating: 57% of the companies surveyed consider that their main LSP has good or very good capability to adapt. Despite this, 42.2% of these manufacturers have a more average evaluation of this capability. Finally, less than half of the agri-food industries consider “the evolution of the logistics service rate” (47.3%) and the responsiveness to the different occasional territory-specific constraints (45.5%) satisfactory or very satisfactory. In short, the mixed perception by the manufacturers interviewed of the intensity of the co-constructed relationship highlights that service packages do not appear to be sufficiently customized and that the proposed solutions are too standardized to respond to the diversity of issues that manufacturers face (just-in-time deliveries, batch splitting, etc.).

Tab. 5 – Evaluation of customization criteria.

|

Criteria on which |

% of respondents with a score between 10 and 8 |

% of respondents with a score between 7 and 5 |

% of respondents with a score between 4 and 0 |

Average evaluation attributed by the manufacturer* |

Standard deviation |

|

General Terms and Conditions of Sale |

22 |

71.6 |

6.4 |

6.55 |

1.34 |

|

Evolution of the logistics service rate of the main LSP over the last 5 years |

47.3 |

52.7 |

0 |

7.55 |

1.04 |

|

Responsiveness to the different occasional territory-specific constraints |

45.5 |

49.1 |

5.5 |

7.28 |

1.53 |

|

Capability to adapt |

56.9 |

42.2 |

0.9 |

7.71 |

1.06 |

|

Responsiveness in the event of a dispute |

37 |

53.7 |

9.3 |

6.91 |

1.47 |

* Ranging from 0 “not at all good” to 10 “very good.

52The third result concerns the manufacturers’ expectations regarding the service package proposed by the LSP (seeTable 6).

Tab. 6 – Main manufacturer expectations.

|

Manufacturer expectations |

% of responses |

|

Provision of operational capabilities |

22.7 |

|

Responsive logistics organization |

18.2 |

|

Innovative logistics solutions |

13.6 |

|

Transparency and rapid flow of information |

10.6 |

|

Customized offering |

7.6 |

|

Controlled rates |

6.1 |

Two items stand out: operational capabilities made available to the manufacturer (proposed logistical routes, storage and transport resources, traceability system, etc.), and the LSP’s ability to respond rapidly to the many issues shippers may face in their daily work. The aim is therefore to offer service packages that meet the operational requirements of customers in terms of volume, deadlines and unforeseen situations. Secondly, it appears that manufacturers expect their LSPs to have the capability to propose innovative logistics solutions that improve existing logistics processes (continuous improvement processes, massification, etc.). These process innovations must increase the efficiency and the logistic performance sought by the manufacturer. It is also noted that in a just-in-time operation context for products with high traceability requirements, the exchange of information on a daily basis is essential: the LSP must be able to ensure that its internal and external network is synchronized in order to guarantee the requested service. On the other hand, customized offerings and rates do not seem to be among the main manufacturer expectations. These criteria were nevertheless cited by the manufacturers in their main expectations.

532.2.2. Determining a typology of manufacturers that identifies

the sticking points of the service packages proposed by the LSPs

In the context of the present study, a principal component analysis was carried out on all the variables allowing the manufacturer to evaluate their main LSP. This analysis made it possible to identify five main dimensions that highly satisfactorily summarize the information (71.6% of the explained variance) (seeTable 7). The five dimensions are: the proficiency in technical and relational skills; the cost of the operational capabilities made available; the responsiveness; the cost of customizing the offering; and proficiency in rate negotiation and development of eco-responsible solutions:

–“Proficiency in technical and relational skills” underlines that manufacturers are looking for LSPs capable of continuously guaranteeing product integrity, of proposing logistics networks of varying density, and of providing a continuous service in terms of product and logistics traceability. In addition, there are relational qualities, which emphasizes the importance of making front-line staff available on a daily basis to respond to the difficulties encountered by the manufacturer when delivering to demanding retailers.

–“Cost of the operational capabilities made available” refers to the basis of the service package mentioned earlier. In fact, the manufacturer simultaneously requires the guaranteed availability of logistic means and customized answers in a very demanding logistic context while still having the possibility of controlling its logistic cost.

–“Responsiveness” confirms the importance given by manufacturers to the LSP’s capability to process orders on a daily basis, the volumes of which are sometimes difficult to predict, and to propose solutions for managing unforeseen events.

–“Cost of customizing the offering” highlights that the LSP must have the capability to develop logistics models that are sufficient to address manufacturers’ specific needs while still being economical.

–Finally, “expertise in rate negotiation and development of eco-responsible solutions” highlights that manufacturers are 54–constantly looking for rates that will enable them to minimize their logistics costs. More eco-responsible solutions, such as the pooling of transport demand, can also be envisaged when they allow economic gains.

Tab. 7 – Rotation of the components matrix*.

|

Components |

|||||

|

1 |

2 |

3 |

4 |

5 |

|

|

NPAbilRealiseService |

.234 |

.783 |

.238 |

-.028 |

.101 |

|

NPTservice |

.128 |

.807 |

.183 |

.266 |

-.028 |

|

NPTariffs |

.042 |

.764 |

.140 |

.163 |

.124 |

|

NPTechnExpertise |

.733 |

.305 |

.121 |

.050 |

.076 |

|

NPQualityRelational |

.721 |

.239 |

.199 |

.158 |

.056 |

|

NPControlTerritory |

.831 |

.011 |

.013 |

-.163 |

-.075 |

|

NPSI |

.707 |

.117 |

-.157 |

.384 |

-.023 |

|

NPReputation |

.794 |

-.074 |

.125 |

-.087 |

.328 |

|

NPEcoEfficiency |

.301 |

.250 |

-.167 |

-.049 |

.775 |

|

Evaluation capability to adapt main LSP |

.101 |

.199 |

.010 |

.826 |

.020 |

|

General Terms and Conditions of Sale evaluation main LSP |

-.048 |

.113 |

.349 |

.648 |

.190 |

|

Negotiating power on the main LSP rates |

-.077 |

-.024 |

.322 |

.283 |

.768 |

|

Evaluation of the responsiveness of the main LSP to the different one-off constraints |

.064 |

.266 |

.800 |

.137 |

.102 |

|

Evaluation of the responsiveness of the main LSP to disputes |

.155 |

.225 |

.830 |

.077 |

-.007 |

* Only structural coefficients greater than 0.5 are retained for each component.

Next, to gain a finer appreciation of manufacturers’ perception of LSPs, a non-hierarchical classification was carried out on the 97 55respondents who provided complete data. The respondents’ profiles were specified according to the five factors measuring the perception of LSPs. To ensure the relevance of the results, a discriminant analysis for each of the typologies created (3 and 4 groups) was performed, and the one with the best reclassification power was retained. Four groups emerged from this classification. The following section will describe and specify them based on the key success factors of the manufacturers’ collaboration with their main LSP, which were the key success factors identified in our survey (see Table 8):

– Group 1 : manufacturers considering their LSP to be a true collaborator. Group 1 brings together almost half of the sample questioned (49.5% of manufacturers). It is characterized by companies that have a very positive perception of their LSP on all the criteria determining the services that the LSP provides. This is reflected in the highest LSP recommendation score of the four groups which is 7.98.

– Group 2: manufacturers seeking operational efficiency and relational quality. Group 2, the smallest group in this typology (9.3% of the sample), brings together, in contrast to the first group, the manufacturers with the poorest perception of their LSP on at least three dimensions (dimensions 1, 2 and 5). This group also low evaluations for dimension 5. In fact, these manufacturers are not very satisfied with the services provided by the LSPs on the first three sources of CVA, which form the basis on which any LSP service package is built: capability to deliver the service, logistics service rate, and rates (the average score on these three criteria is 5.41) and dimension 5 (average: 5.56); the manufacturers are also moderately satisfied with the sources of CVA that constitute dimension 1 (average: 6.44), and with LSP responsiveness (average: 6.44). However, they appear to be satisfied with their LSPs’ capability to adapt as and their General Terms and Conditions of Sale (mean score: 7.22). Finally, it can be noted that the LSP recommendation score is not the lowest of the four groups (6.89).

– Group 3: manufacturers waiting for a customized offering at a reasonable price. Group 3, which brings together a little 56–more than a quarter of the sample (26.8% of manufacturers), is characterized by companies who think their LSPs perform satisfactorily on the basis of sources of CVA and in terms of responsiveness, but less so with regard to customization of the service offering (capability to adapt and General Terms and Conditions of Sale with an average of 6.38/10) and a very low evaluation on dimension 5. Their LSP recommendation score (7.27/10) is slightly below the sample average.

– Group 4: Manufacturers looking for a collaborating LSP with efficient logistics processes. Group 4 (14.4% of the sample) is made up of manufacturers who give below average scores on the sources of CVA in dimension 2 (the base), dimension 1 and customization factors (dimension 4); but above all, they give their LSP the lowest score on responsiveness to the different one-off constraints and disputes (average of 4.75/10). It is these manufacturers who give their LSP the lowest recommendation score (6.29/10).

Tab. 8 – Key success factors according to manufacturer.

|

Group 1 |

LSP is a true collaborator Trust Responsiveness |

|

Group 2 |

Good commercial relationship Responsiveness Pragmatism |

|

Group 3 |

Availability Common objective oriented towards customer satisfaction |

|

Group 4 |

Trust Common objective oriented towards customer satisfaction Genuine willingness from both parties for optimization |

Ultimately, this typology enables us to identify the sticking points that LSPs will have to work on in order to better satisfy their customers. In fact, with regard to the profile of these different groups, it can be noted that the decisive factor in the attribution of a good LSP recommendation score is the responsiveness factor. In fact, the two groups of respondents who give the lowest recommendation scores have two points 57in common: a low score on the “responsiveness” dimension of the LSPs and a low or very average score on the “expertise in rate negotiation and development of eco-responsible solutions” dimension. Sources of CVA do not seem to be the most discriminatory elements in the constitution of this typology.

3. Theoretical and managerial implications

3.1. Theoretical implications

In the highly constrained domain of temperature-controlled transport, the LSP must assemble a number of elements (services and intensity of relationship) to build a relevant service package that meets manufacturers’ logistical requirements (Baranger et al., 2016; Lovelock et al., 2014). Assembling these elements should ensure that the LSP has a complex competitive advantage that their competition will find difficult to replicate (Kacioui-Maurin et al., 2016). This also aims to support the establishment of a long-lasting service relationship with the customer while avoiding any desire on the part of the manufacturer to re-internalize logistics activities. The survey identifies nine items, all of which are sources of added value: technical expertise, capability to deliver the service, logistics service rates, rates, information system, territorial control, relational quality, reputation, and eco-efficiency (see Appendix 1). These items therefore confirm the idea that logistics services are made up of a variety of components, with the service covering the manufacturers’ main requirements in terms of use and utility; it is a standardized logistics service (identical routes, agencies located in the same barycentre, identical lorry fleets, etc.). LSPs prefer a predominance of the mass of transported flows to optimize the infrastructures that will be mobilized to meet manufacturer requirements.

However, when LSPs create highly standardized services based on these nine elements, this raises questions because the present survey reveals that manufacturers want a customized or even innovative response to their logistics needs and the issues they face. Therefore, it is difficult for the LSP to offer a customized service requiring specific and costly 58investments for highly operational services in a sector where margins are low (Dai et al., 2020; Filser et al., 2020; Mevel and Morvan, 2018). These innovation-related difficulties are linked to the work conducted by Busse and Wallenburg (2011) and Bellingkrodt and Wallenburg (2013) who questioned the LSPs’ capability to innovate. At the end of their study, they conclude that that LSPs seem to be less innovative than other sectors of activity, notably because the services they offer are very operational. Conflictual relationships may also be another explanation, as manufacturers are more likely to be “price buyers” than “value-added buyers”.

The level of commitment of front-line staff in the service packages developed by companies in the services field is a very discriminatory factor among customers. However, it can be noted that relational quality, established between LSP and manufacturer employees through the service relationship, is indeed an absolutely discriminatory item for LSPs. Indeed, manufacturers’ perceptions of service quality are highly dependent on the commitment of the LSP’s front-line staff in particular (sales, operations, “disputes” departments, etc.). Establishing a long-lasting service relationship must therefore be particularly supported by a strong interaction with the manufacturers’ employees, which of course requires “business” skills but also relational skills to deal with situations resulting from complex and/or unforeseen customer requests. This relational quality also refers to the service’s collective dimension (improving the circulation of information about customers) such as team meetings, informal meetings, cooperation between individuals with different job types. Front-line staff can thus have a positive impact on customer satisfaction while strengthening the service relationship with the LSP. It should be noted that many studies have demonstrated the influence of the attitudes of front-line staff on customer satisfaction and on their performance in the service provision; the seminal work of Schlesinger and Heskett (1991) in the field of operational management of services is relevant here.

Logistics services are predominantly material services that, like manufactured products, are primarily defined in relation to their intrinsic characteristics and to cost containment. Also, with regard to this important material component implemented by the LSP, most positioning strategies are developed around efficiency, while the strategic service 59triangle, proposes original alternatives likely to promote the emergence of creative service packages. Creative positioning can be found in the airline sector, for example (Ryan Air and Easy Jet as low-cost companies, Delta Airlines for the variety of flights, and Singapore Airlines for customization of the offering). However, LSPs use a standardization approach when creating services to meet manufacturers’ operational requirements. It is therefore essential that LSPs have logistical and informational infrastructures that are capable of delivering by massification all types of products in all national and international directions.

3.2. Managerial implications

The present survey shows that LSPs’ service packages must take into account a set of mandatory determinants to meet manufacturers’ requirements (frequent deliveries from retailer platforms, reduction of delivery times, etc.): capability to deliver the service, logistics service rate, rates, technical expertise, information system, territorial control, relational quality, reputation, and eco-efficiency. More specifically, it appears that the LSP must differentiate itself, through its operational deployment, on the basis of three main criteria: capability to deliver the service, logistics service rate, and rates. The LSP must therefore be able to demonstrate a certain flexibility in the service relationship to offer efficient solutions within the timeframe set by its customer. It must also take into account the requirements and constraints imposed by the end-of-line food retailers4. In addition, the LSP remains the guarantor of an optimum logistics service rate in order to avoid penalties to its customer following delays which, if repeated, can ultimately damage the manufacturer’s reputation with the large retailer. Finally, controlling logistics costs is also essential in the value proposition for a transport whose unit cost remains high because of its specific technical characteristics. Commercial negotiations between manufacturers and large retailers focus not only on product price but also on the final cost of the logistics services. Manufacturers are therefore obliged to constantly reflect on the most efficient logistics solutions.

60Secondly, the perceived quality of the service packages proposed by LSPs is not always clearly superior to the quality expected by these same manufacturers, particularly in terms of the clarity of the General Terms and Conditions of Sale or responsiveness to unforeseen events that can impact their production lines. It follows that the perceived quality of the logistics services packages offered by LSPs is a necessary but not sufficient condition for manufacturer satisfaction. In fact, the perceived value of a given service package will also positively depend on the price paid by the shipper for realisation of the service. However, for the manufacturer, the price paid often seems to be higher than the perceived value of the service as a whole, which tends to weaken the service relationship. Some shippers do not think twice about changing service providers if they receive more attractive rate offers, leading to a certain contractual instability. In terms of logistics services for agri-food manufacturers and supermarkets, the service packages proposed by LSPs positively depend on the perceived quality (CVA)/price ratio, i.e., efficient operational management of services by LSPs for a fair price paid by shippers.

Finally, the proposed collaborative information systems are not considered to be a particularly discriminatory criterion, they appear to be part of the standard service offering required by manufacturers from LSPs. However, the management of physical flows in the temperature-controlled transport field requires LSPs to use information and communication technologies allowing them to collect, process, communicate and store the information that is essential for the routing of these very specific flows. Such a result can be explained by the fact that the information systems deployed between the manufacturers in the agri-food industry and the LSPs have now come of age. Indeed, as the contractual relationship between the manufacturer and the LSP has been strengthened over time, these two actors have managed to develop information systems that are relatively reliable and coherent.

It should be noted that these information systems are based on two very complementary tools: means of transmission (EDI, web EDI, etc.) and means of automatic identification (EAN13, EAN128 bar codes, etc.). They ensure a fast and efficient reconciliation of existing data with previously stored data while performing real-time sorting 61on physical flows (distribution of deliveries, grouping, ungrouping). The possibility to identify products has therefore improved interface management and the overall service relationship established between LSPs and their customers. In short, the development of information technologies has enabled the service provider to offer real-time service packages throughout the supply chain, without any spatial or temporal restrictions. However, the manufacturer has relatively high expectations in terms of the relational quality of their interactions with the LSP. As mentioned above, the importance of human aspects (front-line staff in particular) is what ultimately stand out, and these are put forward by the manufacturer as being a particular guarantor of a balanced service relationship between the parties.

Conclusion

The objective of the present investigation was to identify the components of LSP service packages within food supply chains. We also wanted to define the changes to be considered by the LSP in terms of service production. Based on a survey conducted with manufacturers, it was seen that an LSP’s service package is made up of a set of nine items: technical expertise, capability to deliver the service, logistics service rate, rates, information system, territorial control, relational quality, reputation, and eco-efficiency. Three items also stand out: capability to deliver the service, logistics service rate, and proposed rates. These items must be the basis of any service package offered by an LSP in the temperature-controlled transport sector. It should be pointed out that this service package is too standardized with respect to manufacturer requirements and retailer constraints. Consequently, one of the challenges that LSPs face in differentiating themselves is understanding how to ensure the professional development of front-line staff so that the new interaction, introduced in the production process, is a source of value for the customer. This is important as front-line staff behaviour and skills can be central elements in the manufacturer’s service experience.

62However, there are some limitations to the current study. The choice was made to focus on the food industry5 in one specific territory, however, the work could be extended with a comparative study in several countries in which the food industry has economic clout. Other industries could also be studied. Secondly, the sample is a convenience sample, and therefore the representativeness of the population of manufacturers cannot be guaranteed, even though there is a large sample size. The research conducted offers therefore many extensions. Understanding service quality from the customer’s point of view seems to be a relevant avenue of future research as this it would enable the interaction between the LSP and its customers to be studied in greater detail. Different models and methods for measuring service quality are possible in the specific field of services (Gulc, 2017; Lovelock et al., 2014): Grönroos model (2000), gap model (Lovelock et al., 2014), multidimensional measurement methods (SERVQUAL, SERVPERF, etc.).

The information system has become an essential operational tool for LSPs, enabling them to process more and more quantitative data (Reix, 2002; Scott Morton and Allen, 1995). By becoming a central actor at the heart of multi-actor supply chain management, LSPs generate data sets that are ever larger and varied. This increasingly large mass of data is referred to as Big Data, the control of which is likely to lead to the emergence of new organizational capabilities for manufacturers that are centred around knowledge management and value creation. In view of the contributions and challenges of Big Data, the question then arises as to the consequences for the service packages proposed by LSPs.

63References

Abramovici M. and Suquet J.-B. (2015), “Servuction, qualité de service, et gestion des ressources humaines”, inBesson M., Guéret-Talon L. and Abramovici M. (Eds.), Le cas des services: recueil de cas en management et marketing des services, Caen, Éditions Management & Société, p. 74-79.

Ali S.-S. and Kaur R. (2018), “An analysis of satisfaction level of 3PL service users with the help of ACSI”, Benchmarking: An International Journal, Vol. 25, No 1, p. 24-46.

Baranger P., Dang N ’ Guyen G., Leray Y. and Mevel O. (2016), Le management opérationnel des services, Paris, Economica.

Bellingkrodt S. and Wallenburg C. (2013), “The role of external relationships for LSP innovativeness: a contingency approach”, Journal of Business Logistics, Vol. 34, No 3, p. 209-221.

Blanquart C. and Burmeister A. (2009), “Evaluating the performance of freight transport: a service approach”, European Transport Research Review, No. 1, p. 135-145.

Bonacich E. and Wilson J. (2005), “Hoisted by its own petard: organizing Wal-Mart’s logistics workers”, New Labor Forum, Vol. 14, No 2, p. 67-75.

Busse C. and Wallenburg C. (2011), “Innovation management of logistics service providers: foundations, review, and research agenda”, International Journal of Physical Distribution & Logistics Management, Vol. 41, No 2, p. 187-218.

Camman C., Fiore C., Livolsi L. and Querro P. (2017), Supply chain management et performance de l’entreprise, Paris, ISTE.

Chanut O. and Paché G. (2012), “Stratégies logistiques émergentes: de la grande distribution alimentaire aux réseaux contractuels”, Marchés & Organisations, No 15, p. 91-115.

Cichosz M., Goldsby T., Knemeyer A. and Taylor D. (2017), “Innovation in logistics outsourcing relationship–In the search of customer satisfaction”, LogForum, Vol. 13, No 3, p. 2009-2019.

Dai J., Che W., Lim J.-J. and Shou Y. (2020), “Service innovation of cold chain logistics service providers: a multiple-case study in China”, Industrial Marketing Management, Vol. 89, p. 143-156.

Djellal F. and Gallouj C. (2007), Introduction à l’économie des services, Grenoble, Presses Universitaires de Grenoble.

Duong H.-T. and Paché G. (2015), “Capacité d’innovation du prestataire de service logistique et performance perçue par l’industriel: quelle relation dans le contexte vietnamien?”, Innovation, No 45, p. 137-164.

64Eiglier P. and Langeard E. (1987), Servuction: le marketing des services, Paris, McGraw-Hill.

Elten B., Landry T. and Daugherty P. (2010), “Investigating the influence of velocity performance on satisfaction with third party logistics service”, Industrial Marketing Management, Vol. 39, No 4, p. 640-649.

Fabbe-Costes N. and Roussat C. (2011), “Supply chain integration: views from a logistics service provider”, Supply Chain Forum: An International Journal, Vol. 12, No 2, p. 20-30.

Fattam N. and Paché G. (2017), “4PL intermediation: exploring dimensions of social capital”, inSaglietto L. and Cézanne C. (Eds), Global intermediation and logistics services providers, Hershey (PA), IGI Global, p. 64-85.

Filser M., des Garets V. and Paché, G. (2020), La distribution: organisation et stratégie, Caen, Éditions Management & Société, 3rd ed.

Fulconis F. and Saglietto L. (2015), “Intermédiation logistique et pilotage des supply chains: de nouvelles responsabilités pour les prestataires de services logistiques (PSL)?”, inPardo C. and Paché G. (Eds.), Commerce de gros, commerce inter-entreprises: les enjeux de l’intermédiation, Caen, Éditions Management & Société, p. 101-122

Gadrey J. (1996), Services: la productivité en question, Paris, Desclée de Brouwer.

Grönross C. (2000), Service management and marketing: a customer relationship management approach, New York (NY), John Wiley & Sons.

Gulc A. (2017), “Models and methods of measuring the quality of logistic service”, Procedia Engineering, Vol. 182, p. 255-264.

Hiesse V. (2015), “L’intermédiation dans les canaux de distribution: quels schémas émergents?”, Logistique & Management, Vol. 23, No 4, p. 79-91.

Jolibert A. and Jourdan P. (2011), Marketing research: méthodes de recherche et d’études en marketing, Paris, Dunod.

Kacioui-Maurin E., Lazzeri J. and Michon V. (2016), “L’innovation des prestataires de services logistiques (PSL): une analyse par les comportements stratégiques”, Logistique & Management, Vol. 24, No. 2, p. 86-97.

Lovelock C., Wirtz J., Lapert D. and Munos A. (2014), Le marketing des services, Paris, Pearson, 7th ed.

Mehmann J. and Teuteberg F. (2016), “Understanding the 4PL approach within and agricultural supply chain using matrix model and cross case analysis”, International Journal of Logistics: Research & Applications, Vol. 19, No 5, p. 333-350.

Montebello M. (2003), Stratégie de création de valeur pour le client, Paris, Economica.

Mevel O. and Morvan T. (2010), “Prestation logistique en produits frais et mesure de la valeur ajoutée client: le cas des industries agroalimentaires bretonnes”, Revue Française de Gestion Industrielle, Vol. 29, No. 3, p. 47-74.

65Mevel O. and Morvan T. (2011), “Le système d’information est-il toujours reconnu comme un avantage concurrentiel permanent et autonome pour le PSL? Le cas des outils de traçabilité dans les filières agroalimentaires fraîches et ultra-fraîches”, Revue Française de Gestion Industrielle, Vol. 30, No. 4, p. 47-74.

Mevel O. and Morvan T. (2018), “Le PSL, variable d’ajustement ou partie prenante dominante à la relation industrie/commerce? Le cas des produits frais et ultra-frais dans le Grand Ouest de la France”, Logistique & Management, Vol. 26, No. 4, p. 256-274.

Olah J., Karmazin G., Peto K. and Popp J. (2018), “Information technology developments of logistics service providers in Hungary”, International Journal of Logistics: Research & Applications, Vol. 21, No 3, p. 332-344.

Reix R. (2002), Systèmes d’information et management des organisations, Paris, Vuibert, 4th ed.

Saglietto L. and Cezanne C. (2015), “Redefining the boundaries of the firm: the role of 4PLs”, International Journal of Logistics Management, Vol. 26, No. 1, p. 30-41.

Schlesinger L. and Heskett J. (1991), “The service driven company”, Harvard Business Review, Vol. 69, No 5, p. 71-81.

Scott Morton M. and Allen T. (1995), L’entreprise compétitive au futur: technologies de l’information et transformation de l’organisation, Paris, Éditions d’Organisation.

Sohn J.-I., Woo S.-H. and Kim T.-W. (2017), “Assessment of logistics service quality using the Kano model in a logistics-triadic relationship”, International Journal of Logistics Management, Vol. 28, No 2, p. 680-698.

Volle M. (2000), E-économie, Paris, Economica.

Wagner S. and Sutter R. (2012), “A qualitative investigation of innovation between third-party logistics providers and customers”, International Journal of Production Economics, Vol. 140, No. 2, p. 944-958.

Wallenburg C. and Lukassen P. (2011), “Proactive improvement of logistics services providers as driver of customer loyalty”, European Journal of Marketing, Vol. 45, No 3, p. 438-454.

Zacharia Z., Sanders N. and Nix N. (2011), “The emerging role of the third party logistics provider (3PL) as an orchestrator”, Journal of Business Logistics, Vol. 32, No 1, p. 40-54.

66Appendix 1

Profile of the manufacturers interviewed

Breakdown by activity segment

|

Percentage |

|

|

Meat industry |

32.4% |

|

Dairy industry |

23.4% |

|

Prepared meals industry |

11.7% |

|

Seafood industry |

10.8% |

|

Fruit and vegetable industry |

8.1% |

|

Bakery and Pastry industry |

4.5% |

|

Confectionary and Chocolate industry |

3.6% |

|

Other industries (egg products, animal feed) |

5.4% |

|

Total |

100% |

Size of businesses questioned

|

Percentage |

|

|

Very small business |

9.3% |

|

Small- and medium-sized business |

62% |

|

Intermediate-sized business |

25.9% |

|

Large-sized business |

2.8% |

Breakdown by region

|

Percentage |

|

|

Normandy |

35.8% |

|

Pays de la Loire |

35.8% |

|

Brittany |

28.4% |

Appendix 2

Definition of the different sources of customer value added (CVA) identified

|

Technical expertise |

|

The LSP’s professional skills as regards its ability to demonstrate its complete technical expertise in the field of temperature-controlled transport for fresh and ultra-fresh products, and its professional experience in the cold trade. |

|

Capability to deliver the service |

|

The LSP’s positive response rate to the expectations of the agri-food industries in terms of capability to respond to an array of requests for service provision (collection, storage, splitting, transport, etc.). |

|

Logistics service rate |

|

Measure of the LSP’s capability to respond quickly to a request, and to produce a quality service provision respecting the flow set out, deadlines, and price quoted. A high logistics service rate minimizes dispute rates with the manufacturer. |

|

Rates |

|

The LSP’s price positioning is measured here through its capability to make commercial efforts while maintaining rates levels in line with those of the competition. |

|

Information system |

|

The capability of the LSP to implement, with the manufacturers, common and scalable technology for data transmission (delivery schedules, volume, weight, etc.) through a collaborative work platform operating under the EDI standard and likely to offer a pre-invoicing service. It also covers logistics traceability as a tool for the transmission and identification of standardized data based on automatic means of identification. |

|

Territorial control |

|

The regional, national and international geographical reach of the LSP. In the present study, this is considered through the manufacturer’s consideration of all resources (physical locations, organizations, etc.) and skills (human qualifications) their service provider uses at the local and global level to develop a networked system of agencies or various sites and which are likely to promote a high value-added service relationship in a win-win approach. |

|

Relational quality |

|

The evaluation of the quality of human exchanges in commercial matters, both in the offices (front-line staff, negotiations, dispute settlement) and on the physical logistics platforms between staff (drivers, etc.). |

| 68

Reputation |

|

This indicator globally qualifies the LSP’s brand image in the eyes of the agri-food industry in terms of its reputation it has built up in the profession compared to the competition. |

|

Eco-efficiency |

|

The image of the LSP retained by the manufacturer for the design and implementation of a green supply chain, i.e. an inter-company relationship oriented towards a more environmentally friendly service provision. |

1 The basic or main offering is what the customer expects to find, and if this is missing, they will be completely dissatisfied. Additional or peripheral services have the function of building customer loyalty.

2 These criteria emerged following a series of semi-structured interviews that had previously been conducted with logistics managers.

3 In our sample, 31% of the manufacturers have been working with their main LSP for over 20 years.

4 For example, some of the agri-food industries interviewed distinguish five flows in their logistics organizations: early flows (ordered the day before), day flows (ordered the same day), small flows (small orders), specific flows (delayed differentiation), very urgent flows.

5 The agricultural and food industry represents 15% of GDP and 10% of exports in France, it is the third largest sector in terms of trade surplus (after aeronautics and cosmetic chemicals).

- Thème CLIL : 3306 -- SCIENCES ÉCONOMIQUES -- Économie de la mondialisation et du développement

- ISBN : 978-2-406-12261-6

- EAN : 9782406122616

- ISSN : 2555-0284

- DOI : 10.48611/isbn.978-2-406-12261-6.p.0035

- Éditeur : Classiques Garnier

- Mise en ligne : 27/10/2021

- Périodicité : Semestrielle

- Langue : Anglais

- Mots-clés : valeur ajoutée pour le client, prestataires de services logistiques (PSL), bouquets de services